Yes I agree Lord @Porridge, it’s the High Street mob that have lost the plot. 30-40 years ago they were OK, but since then it’s been a slide into oblivion.

I do have an account with First Direct, just as a backup, but I do all my own actual “banking” with Nationwide Building Society.

We had to open the Lloyds account for my Dad’s trust as at that time very few financial institutions would allow accounts for trusts, and the number is even smaller now.

UK Banks will be first up against the wall when the Revolution comes, closely followed by insurance companies.

Make sure you demand daily interest at standard deposit rates to be paid to you for every day of the delay in addition to the principal. I’d make it clear in writing I presented myself or was at least available, to collect the funds in-branch on the date of the closure and instead they have made your money become inaccessible to you. You therefore demand that interest will accrue and be paid to you for every day beyond the date of closure that the money is unavailable to you. Send them notice in writing or make them sign a receipt for tbe letter at the branch.

If I could I’d demand it all (principal + interest) to be handed to me in cash at the branch as well. Bvggvr their policies.

Have you read up on a complaint you could make to the Banking Ombudsman if there is one? The FOS isn’t my fave, although a FOS complaint does cause the bank to have to pay the FOS a fee to process it (a few hundred £££ but Lloyds will probably have a season ticket for this that gets them a reduced rate.)

There’s a website called something like ceoemail that I’ve used in the past. It worked with Barclays and Booking.com, possibly others that I’ve forgotten.

I placed an order for blinds of various types for our new house.After getting various supply and fix quotes decided to go on line supply only. Easy to fix and the same quality.

The order came in 3 parts, roller blinds, venetian blinds and finally ‘perfect fit’ blinds for our bi-fold doors.

The measuring instructions were explicit on the companies website which I followed to the letter.

Roller and venetian blinds fitted perfectly but not so the ‘perfect blinds’, they had been made to exact size without tolerance.

I studied the manufacture and could easily see their error.

I spent 5 weeks and many emails passing back and forth from their complaints department witout satisfaction.

With some research I found the MDs email address and copied him in to all the previous complaint emails which I did over a weekend.

By 9.30 the following Monday morning I had an extremely apologetic email from the complaints department, of which there was no doubt it was instigated by the MD, confirming a full refund plus extra for the buggerance factor.

I had also told them that I would return the ‘perfect fit’ blinds as long as they paid the postage.

They told me to donate them to charity instead!

It took me around 4 hours to make the necessary adjustments to the blinds which are now a ‘perfect fit’.

Result!

This is why I dumped high street banks for fintechs a decade ago. Emailing anne@starlingbank.com, tom@monzo.com or nic@revolut.com got you a reply to your issue within hours, and from the actual CEO, not some ‘Exec comms team’ or such like in a high st bank, you had an issue with your Starling account and Anne the founder was replying and getting it sorted, at one time within 15 minutes of sending it! They’re all bigger now, and Anne and Tom have moved on from the banks they founded, so things are less immediate, but for years the customer service was at a level that even those with a few million in the bank would be envious of.

The finale to this saga (and I will try and keep it brief!)

Once my 28-day waiting period was up I re-entered the hallowed portals of Lloyds Bank in Guildford.

After much probing, the lady I spoke to said that the money was being held at Head Office - the powers that be had changed their mind about sending cheques out to pay off the closed accounts, and were instead just sitting on the money and waiting for us to come and claim it!!!

She of course had no power to hand over the dosh, but promised to put the branch manager on the case, whose name she gave me.

Of course you can’t phone or email these people, so as a week later I had heard nothing I went in again.

On this occasion I got to see the manager, the sainted Rhona Duckett, who was finally able to help me. She was quite apologetic and said she was dealing with several similar cases.

Anyway by using the Force or some kind of Hogwarts-derived magic spells, she extracted the money from Head Office and got it sent to Guildford, and a couple of days later I was able to go in (again!) and collect a cheque, with which I hastened to Metro Bank and got it paid in.

She offered me £50 compensation and £42 to cover my expenses - somewhat derisory but by this point I just wanted to never have to darken their doors again.

As I mentioned in another thread, if you want customer service from your bank, invest in a biscuit tin under the bed…

You absolutely must demand lost interest - as had they been prompt and not disorganized and poorly communicating you could have invested it elsewhere for the time they wasted. Plus a compensatory payment for inconvenience, stress or sheer bloody-mindedness.

They are most definitely in the wrong here in terms of level of performance and you have had losses.

£92? They’re having a laugh, with the sums involved. I’d have also mentioned mileage costs at HMRC rates for each extra trip to bank should be refunded. Might not be much but the rate must be 60p or so now per mile? but it’s the principle.

Thank you for your concern and sympathy, and in principle I agree, but it’s really not worth the effort.

If the Trust earns interest it will have to do UK tax returns which is not worth the hassle. My mother is 101 in August so it’s very likely that the whole thing will be wound up in a year or two at the most.

I have enough going on at the moment trying to keep her safe at home while I sort out a care home, with zero help and lots of back-seat driving from my siblings, so the last thing I need is extra admin work right now.

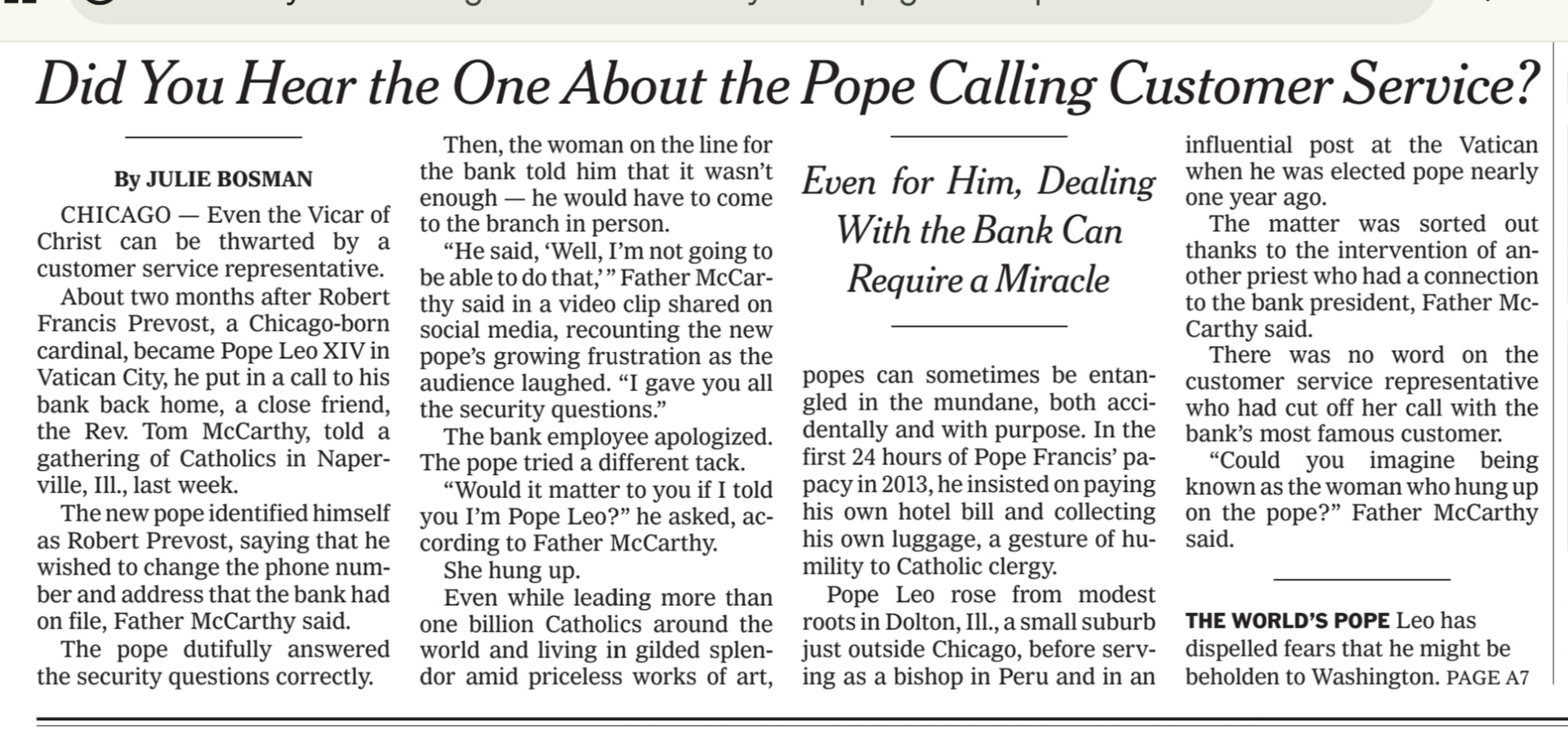

I’m not sure if it’s depressing or reassuring to learn that even the Pope recently struggled to persuade his (US) bank to change his phone number and address..

Surely the Pope should use the Vatican bank? They do issue VISA cards apparently…

The Vatican Bank (Institute for Works of Religion - IOR) offers Visa cards to authorized account holders, providing secure, international payment capabilities with 3D Secure.

These, along with other debit cards (Bancomat), are specifically linked to IOR accounts for use within Vatican City and on global Visa circuits.