This is incredible - you’re following almost exactly the same though pattern as myself!

500k was just to simplify the calculations for my ageing brain … … …

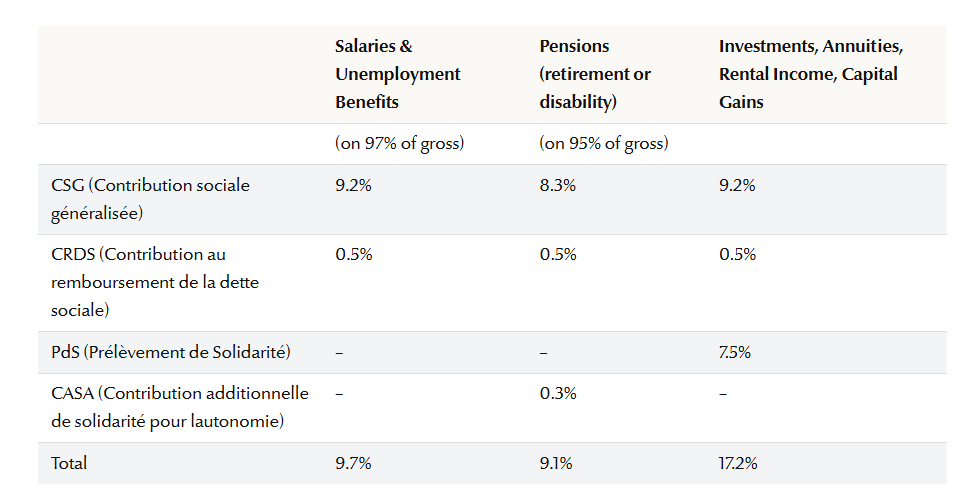

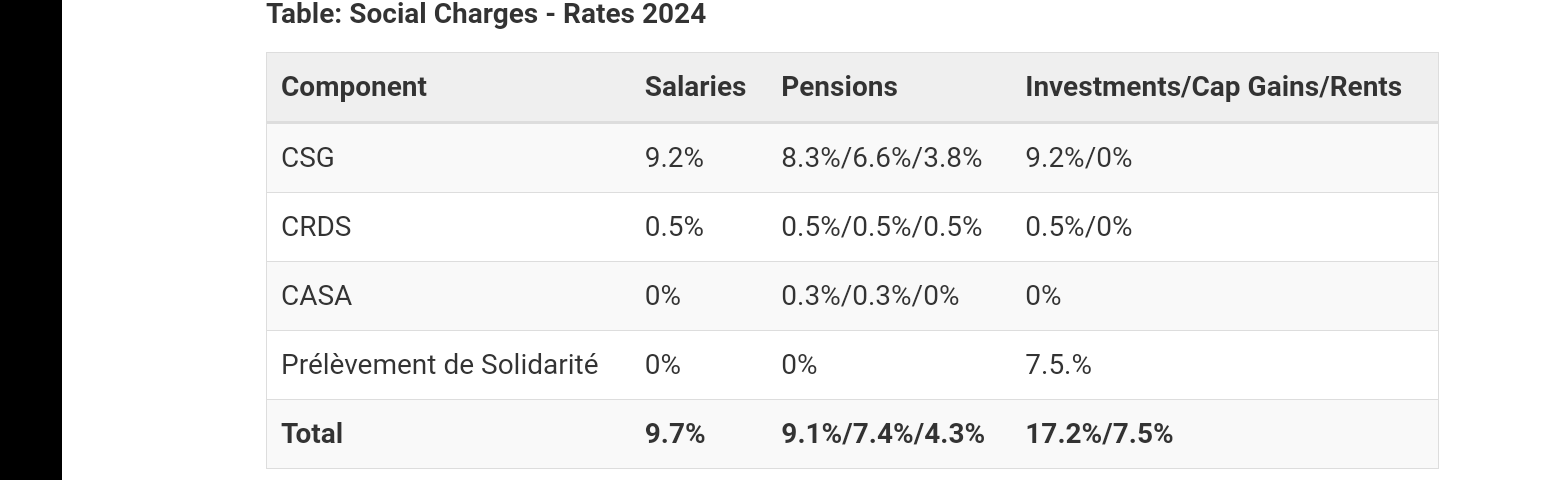

So - not sure if you’re British or receive S1 - but I believe what I’ve learned is that (strictly for Social charges) we have to pay CSG + CRDS ~8.5% and PDS ~7.5%

Now - I think up until getting form S1 we have to pay CSG+CRDS for ~70% healthcare cover and then acquire a private mutuelle to top up to 100% cover. However, I think you’re suggesting that if we use a mutuelle for 100% and opt out of healthcare - then we escape having to pay CSG+CRDS at all.

However - presumably you still do need to pay the PDS at 7.5%?

I went into a tax office in France to sort all of this out - and they were VERY nice but told me that the the Social Charges were a mystery to them.

So - potentially if we pay for 100% private health care then our Social charges drop from 17.2% to 7.5% on pension drawdown.

I’m really sooooooo interested in this idea - but do you know how much it costs (very approximately) for 100% private health cover?

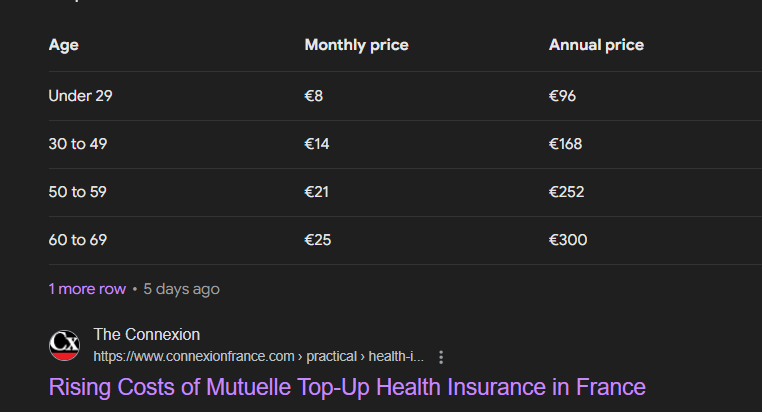

I’m guessing that a top up mutuelle comes in at the lower end at £50 per month so if that’s 30% cover, then 100% should be around £150 per month.

Does that all sound logical?

I guess 100% private healthcare can be bought from the same companies that do the top up mutuelles?

Not a mutuelle (which is the top up insurance) but full private health insurance. You get it from big profit making insurance companies like Axa and Cigna. Costs are more in region of €500 a month. You are obliged to get full coverage to be acceptable for a carte de séjour.

Mutuelles are in the true sense not-for-profit and are highly regulated. Only people with a French social security number can get one, which means only if working or partipating in the syatem. A €50 a month mutuelle doesn’t get you much if over 50.

No, CSG is variable according to type of income and gies up to 9.2%. In total without exonerations for not being in French Social Security it can be uo to 19.2%.

CA-Britline were nice - thinking though of looking at the new players in the field.

I think we can get free debit card/visa card/account with Boursorama.

When I find out more - will post back here so some of the guys on this site can save some money.

I’ve also heard of a company called Fortuneo - so will probe deeper there!

On top of all of the Banking/Internet changes in France - I’ve been really impressed with Dacia and Citroen coming out with e-cars at E15k - E20k … … we’re definitely going to be putting in solar panels/battery in Foix and try and go offgrid-ish … … I’m assuming that solar is doing well in France - given that the country has sun!

Thanks Jane - eeeek! So E12k for private cover for myself and wife … … that’s a lot! We’ll probably just go with paying CSG+CRDS then and getting a cheap as chips top up mutuelle.

I don’t know if this kinda’ information is correct … …

The connexion is used to light our fire. Nothing else.

A cheap as chips mutuelle will not give you a return. We had one to start with and being in reasonable health with no major eye or teeth issues we paid out c€300 a year to get maybe €50 back. You need to look at your personal circumstances and risk appetite.

We now have a hospital only policy and pay the rest of the “part mutuelle” ourselves. It works out at a saving of approx €1000 a year.

Hi apologies for seeking clarification - does that mean that you’ve upgraded your top up mutuelle from bargain basement to a higher level (that is upgraded the top up part) or actually opted for 100% private insurance?

Can I ask how much the monthly payments changed to get decent coverage?

I’ve seen something about the top up mutuelle coming in different prices based on differing levels of cover - where exactly as you say … … you don’t get much for the cheapest mutuelle but it at least satisfies the rule in place that people can’t enter France without 100% health cover.

It looks like it’s not tied to taking any other service - eg i/net but their €19.99 p.m. for basic fibre i/net is the cheapest I have seen. ‘Boogie’ seems to have a decent reputation.

I was certainly impressed by the Eng lang talk-thru’ of the sign-up process. I started off with a woman who was probably Easten european. After muddling along she went off and got a bloke with excellent Eng and probably in a senior pos’n. All went perfectly well from that point.

When I was called back next day, as promised, I think it was a different guy but with the same standard of Eng.

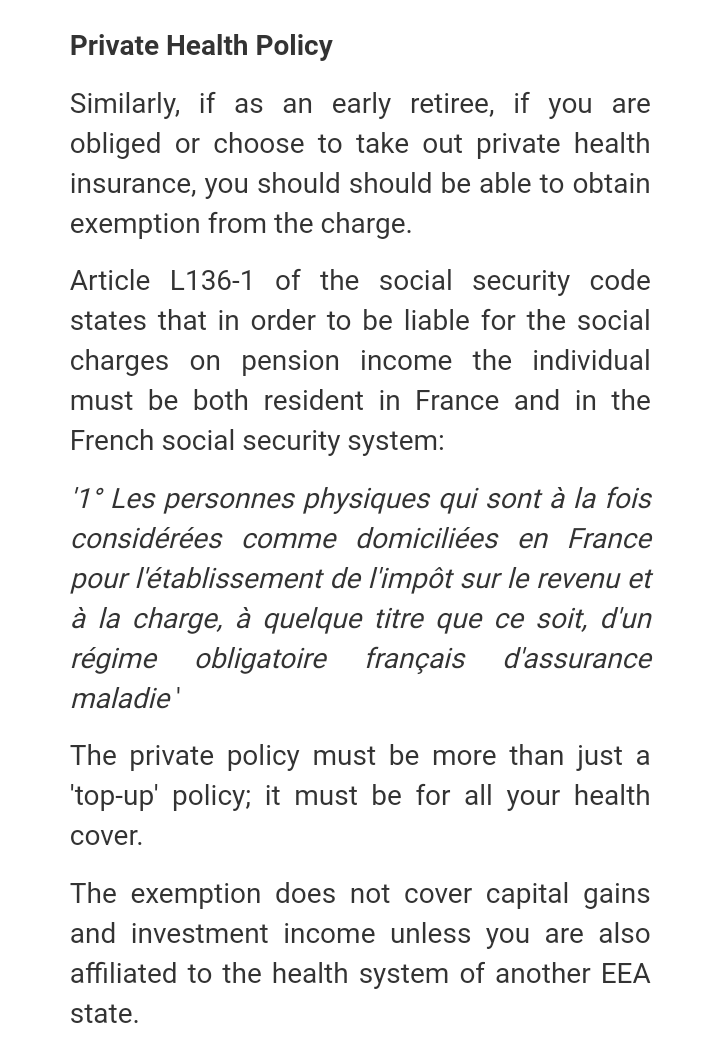

It can be hard to get your head round the French Health Service as it is based on such entirely different concepts.

To live here you have to have Health Cover at the same level as a French resident. Which does not cover 100% of costs as French Health cover is participative. You can get this cover either by joining the French Health service after you have been here for a while, having and S1, or taking out full private health insurance.

Depending on circumstances joining the health service may not be free, but is affordable and very good value.

For the visa I think you need PHI now and having an EHIC/GHIC is not acceptable for visas over 6 months.

Once actually here and getting to end of your PHI cover it is then your choice as to how you cover the remaining costs, either via top up insurance (mutuelle) or from your own pocket. The cost of a mutuelle is based on your age and the level of cover you want. However the basic 100% mutuelle may not actually cover 100% of the costs because of the way the reimbursement system works.

There is a specific cost and reimbursement for each medical act, from bandaging a finger to cardiac bypass. And some things the reimbursement is much, much less than the actual cost so getting a 100% reimbursement is peanuts

But in general the places where costs can skyrocket is in hospital. A simple colonoscopy can cost €4000. So we have chosen a policy that only pays out if we are in hospital, and will pay costs that are way over standard reimbursement.

All of this is a personal choice which you don’t need to bother about to start with as you coukdn’t get a mutuelle anyway!

There should be NO social charges whatsoever on your pension, whether lump sum or regular withdrawals, if you are privately insured for medical. Each year we tick the appropriate boxes on our French tax return to confirm we are not in a French compulsory social security regime.

I’m a Brit. No S1 due for several more years (I’m 61).

We pay 3250€ a year to AXA International (in London) for worldwide hospital cover + cancer treatment (excluding the US!) with a high excess to reduce the premium. In practice we pay ourselves for our routine medical costs eg doctors fees, medicines etc. The proof of the pudding was that AXA paid for a week’s worth of intensive care, well above the excess in 2023. We absolutely do not insure for 100% cover - that would be extremely expensive, and we believe unnecessary for us.

French insurers didn’t want to cover us, as my wife had a preexisting condition even when we offered to waive any claims for the condition. So we turned to the international market which was far easier to navigate, and had numerous offers.

What I am suggesting is that a lump sum from a UK pension scheme for a French tax resident would be taxed at 6.75%-7.5% (there is a capped 10% allowance for foreign pensions which makes the rate closer to 6.75%). If combined with private medical cover there are then no social charges. If you go for the regular drawdown route, the tax rates would be higher, but still probably much less than UK tax rates (including 10% allowance as above) especially if you are married (given France’s generous tax treatment of married couples) and no social charges if privately insured for medical.

Thanks to you that’s Phone + Internet covered.

Lovely!!!

Bit of an Internet forum junkie here! and lovely to find a couple of services that’re cheaper than the UK.

Thanks Capn!

(I won’t mention my allegiance to Man Utd and City over the 70s and 80s - Liverpool were something else back then with the Kevin Keegan dream team; used to live on Maine Road).

Hi George, would it be possible to ask what your excess is? and if you plan to jump back into the French health system with S1?

I guess the bit that I’m struggling with in your post is that I can understand how CSG + CRDS can be escaped - but I’m a bit confused re:PdS.

Originally when I started research I was told that you get absolutely nothing for the Social Charges.

Then it transpired, that they’re essential for entry into the standard French healthcare system (paying 70% costs)

… … but I’ve never come across any means of avoiding the PdS at 7.5%.

If you look at that image I’ve attached above.

You’re right in that there is no PdS on Pensions.

But I think I’ve been told (by non-experts) that the UK private pension before formal retirement at 65/67 is considered an investment (where PdS is payable) not a pension (where PdS isn’t payable) because the private pension doesn’t as such exist in France.

Does that make sense? Personally I thought it was a bit silly if an inactive living on something called a pension, was not treated like an inactive on a pension.

Hi George1 - just thinking about it - if we were to take the whole pension in 1 go on a full private healthcare setup like yours, we could then get the sum minus ~6-7% flat rate tax - pop the money into Nalo … … … and then opt back into the standard French healthcare system the year after escaping that one-off Social Charge!

(Feeling a bit naughty but it all sounds acceptable!)

EDIT – Looks like it’s standard practice to avoid the Social Charges.

I have to admit that these couple of days on SurviveFrance have been a revelation.

(I don’t think I have any more questions at all!!)

-*-

Here’s a link to George1’s comment.

If you withdraw your entire pension in this manner, you will receive a 7.5% fixed rate, after a 10% allowance that is not capped. With French tax rates reaching up to 45%, plus possible social charges levied on your pension income (see above), this could result in significant savings, allowing you to reinvest the capital in France.

A critical point to remember for UK retirees is that the entire pension pot must be taken in one payment (see point 2 above). When reaching pension age, UK residents can withdraw up to 25% of their pension tax-free, and many retirees do so before moving to France (after which the tax-free option becomes irrelevant as you would no longer be a UK tax resident). However, doing so would eliminate the fixed-rate tax option.

from sjb global

For all these variations of health insurance Fabien (you can PM him with just @ in front of that name) is a friend of the site and his team are excellent and can quote and advise on these options.

Also as an illustration to reinforce jjones’s point, policies may have options to take, say 300% dental cover and you might still be a chunk away from the actual cost of treatment due from you.

I’ve also noticed a lot of Brits still get glasses for eyes etc in the UK rather than including cover for that here in France as costs can remain much higher here even with coverage but that may be Brits with an S1 ie retain rights in UK as well.

I will try to answer your various additional questions in turn below…

€2550 per person (I’m married)

Exactly that, once the S1 is accepted and I have transferred all the amounts withdrawn from my UK pension funds to Nalo.

My understanding - I defer to far more knowledgeable people on social charges on SF - is that the Prélèvement de Solidarité (PdS) is not due on pensions, but applies to investment income eg rents, interest, gains etc. Extract below seems to confirm this…I also include the chapter and verse on the rationale for being exempt from social charges.

I’m with First Direct, which is a division of HSBC UK. I had the account prior to moving and they have changed my official address to my French one and send codes to my French phone. Like some others, they won’t open an account if your not UK registered but are happy for you to keep an account if you move to the EU.

Children and the over 60s get free eye tests in the UK but the cost of glasses is not covered by the NHS, though there are some vouchers available to help with the cost for people on benefits or who need an unusually strong prescription.

I think that people coming back to the UK for specs probably has more to do with the competitiveness of the market. My last set of specs which are fairly up-market (three zone varifocals with thin lenses and anti-scratch and anti-reflective coatings) were about £330.

You can get optical cover on private health insurance I believe, though I don’t know if it’s cost-effective.