Super interesting as a first time poster, and having waded through many websites (SL, Blevins, IFA, Impots, QROPS, french-property). This is the first time someone has confirmed for me that Charges social are not applied when taking a lump sum (PFL) from a non-FR pension. @George1 ! thank you very much. I have three questions on it if I may 1) Is there anything that you need to ‘do’ actively with the French impot in terms of ensuring that CSG is not taken out by them at time of filing… and 2) If this is not too personal, what residency were you under at this time ? (CdS ? multi-year? citizen?) and lastly 3) which health insurance provider have you used ?

(Asking as I am UK citizen, but with CdS 1yr, and a French wife, debating if citizenship makes this path more complex/harder as I think you might automatically qualify for CPAM after 3mths in Fr)

I also have pensions >LTA so am querying the appropriate path on a pre/post Labour victory.

Very high quality discussion and polite. Feel like I have stumbled into a friendly pub! Thank you all contributors

Welcome Andy. I’m sure the contributors to this thread will very much appreciate your kind words.

You raised some questions after (I suspect) reading the below…

1). Yes. You simply tick boxes 8RP and 8RQ on your return (assuming it’s you and you wife) to confirm you are not affiliated to a compulsory French medical insurance regime… That is key.

2). I’m a UK citizen on a 5 year EU family member CdS, as I’m fortunate enough to be married to an EU citizen (from Luxembourg)…

3). We use AXA as they were affordable (we wanted a high excess - 2500€ - to drive down the premium costs), very responsive, generous with discounts we hadn’t even asked for (!) and very relaxed about prior medical conditions… The plan we use is the Global Health Plan EU (excl the US). Premiums are about 2750€ a year for the two of us, and in essence are for the really serious things like hospitalisations, cancer treatment etc.

We were turned down flat by a number of French insurers, but several international insurers based in London were more than happy to write the business.

In practice we pay for all routine doctors consultations and medicines, and are working on the view that premiums plus medical costs are less than the prélèvements sociaux that would otherwise arise on some pensions coming to France. The savings will obviously depend on the quantum of the pensions lump sums due. This is a position that I suspect is fairly niche. Many would probably not be comfortable with absorbing the health, peace of mind and financial risks involved, and/or able to afford being outside Assurance Maladie, particularly if they have costly, significant medical conditions.

For the time being we are in excellent health, but I’m touching wood furiously as I type this. Our aim is to switch to Assurance Maladie in about 5 years, once we’ve ‘run off’ our personal pensions.

If you’d like to discuss any of this in more detail, I’d suggest using the PM route…

Finally on LTA, I’m working on the reasonable assumption that the same current limits and restrictions might be revived if Labour actually reintroduce it, as opposed to threatening to introduce it. I’d dearly love to accelerate a DB pension ahead of any changes in government,but the discount imposed for early access is punitive and probably isn’t worth the risk.

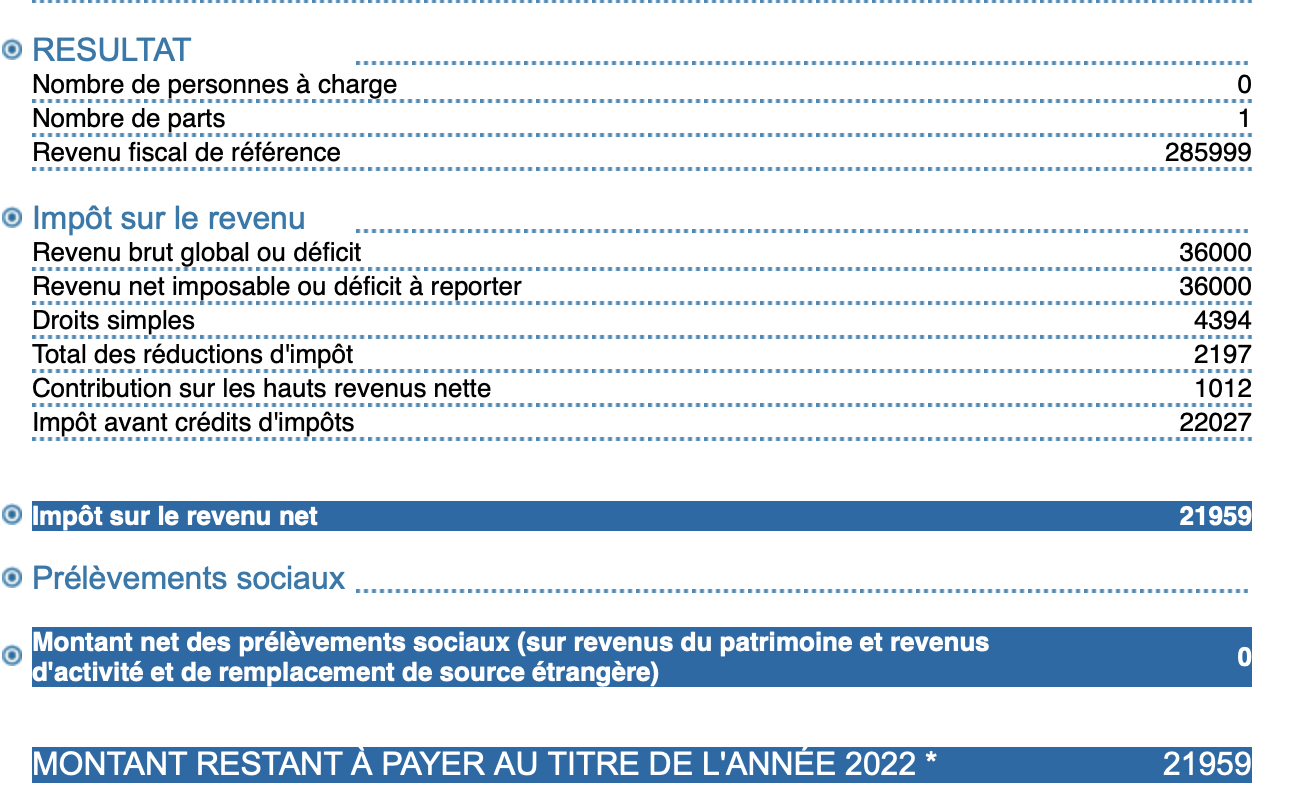

I’ve just discovered that lump sums declared at the 7.5% flat rate are added to the reference revenue fiscal - and that could lead to some exposure to the ‘Contribution sur les hauts revenus’.

Most like me will not have heard of this tax, not normally being in that income level. Here’s the rates…

Fraction de revenu fiscal de référence

Taux pour une personne seule

Taux pour un couple soumis à imposition commune

Jusqu’à 250 000 €

0 %

0 %

Entre 250 001 € et 500 000 €

3 %

0 %

Entre 500 001 € et 1 000 000 €

4 %

3 %

Plus de 1 000 000 €

4 %

4 %

So lump sums totalling €277777, after the 10% reduction will be 250K. That will for a single person result in the 3% extra tax being applied to their other income. This high income tax even seems to be applied to non France taxable pensions such as UK government pensions. Though maybe the simulator might be wrong. Obviously higher levels of lump sum will get charged as well.

This won’t make a massive change to the case for using the flat rate for pension lump sums but might be something for people to bear in mind if they have e.g. several pensions reaching these sorts of levels.

Here’s the output from the simulator for 277777 lump sum and 20K France taxable pension and 20K government pension.

PS I found this out because I thought to test what the simulator calculated for social charges for lump sums - it kept coming out at zero and I thought maybe we needed a large amount for social charges to kick in. But the simulator doesn’t calculate social charges for pensions, except for interest and rent.

That approach would be consistent I guess with UK government employee pensions being taxed in the UK, and yet even if no tax on them is payable to France, their gross amount is still added to any other income from anywhere by France in calculating tax due. Which may well push you up into a higher tax band in France even if the UK government pension part of it wasn’t subject to tax in France.

Accidentally finding oneself in a higher tax band might also presumably affect eligibiity for other things - or expose to things such as wealth surcharges of some sort depending what else happened in the same calendar year? and not just tax, too.

That’s excellent research. I agree it shouldn’t change the general approach of seeking the 7.5% tax rate on pension lump sums, even quite substantial ones.

I see from the guidance material online that there is a helpful form of transitional relief, (using the ‘quotient’ or ‘top slicing’ approach). It applies for those taking a lump sum that is equal to or more than 1.5 X their previous two years average income, and reduces the special tax charge.

.

I used the quotient approach for one pension pot (from which I had already made several drawdowns in the UK). It was not a big pot, but this was the first (paper) declaration in France, so probably the ratio to previous income did not apply. It was accepted by the Impots.

We fixed our date of arrival in France as 26 Feb 2019 for change of residence.

I stapled on a supplementary paper explanation of what I had done,

Les feuilles de papier supplémentaire agrafée à cette déclaration.

in this regard:

7) AVIVA pension - une prestation de retraite de R.U. servie sous forme de capital reçu en 2019 depuis le 26/02/2019. Deux paiements: l’un de xxxx£ brut le 03/04/2019 (au cours de la dernière année d’imposition au Royaume-Uni) et l’un de xxxx £ brut pris le 31/05/2019. Le deuxième versement a mis fin à cette pension. En total 21457 .21 euros, donc déclaré sur le formulaire 2042 C, à imposer selon le système du quotient, boîte ØXX. (HMRC a remboursé la taxe reçue le 05/11/2019. Les sommes sont donc déclarées brutes.)

We did also, right or wrong, claim the 7.5% for other pension pots. We had paid Blevins Franks for advice, and that accorded with their advice at the time. That was also accepted as:

8) ELEVATE Pension - une prestation de retraite de R.U. servie sous forme de capital - un seul paiement effectué 29/05/2019 qui a terminé cette pension. Cette somme de £xxxx brut, Euros xxxxx, est déclarée sur le formulaire 2042, Option pour le prélèvement libératoire de 7,5 %, boîte 1AT. (HMRC a remboursé la taxe reçue le 05/11/2019. Les sommes sont donc déclarées brutes.)

That’s really helpful information, thank you for posting the details. The disclosure notices also look to be models of concise, relevant information from the tax authorities point of view. As an aside, I’m impressed at the speed (by HMRC’s usually fairly low standards) with which you’ve evidently persuaded HMRC to refund you the tax. I recall an earlier post from you on how you ‘manage’ HMRC’s technical specialists, to encourage them to pay up asap.

One detail intrigued me.At the end of each disclosure notice there is reference to the amounts declared being gross, after refunds of tax withheld by HMRC. From a professional curiosity point of view, I wonder what Blevins would have advised reporting IF HMRC hadn’t speedily refunded the tax within the same calendar year (if indeed the issue was actually discussed)? For the benefit of others reading this, it was entirely correct and appropriate to report the gross (ie full amount of) income, (as you did), even if HMRC hadn’t refunded the tax in the same year. I appreciate this looks like it all happened 4-5 years ago, so please don’t go to any trouble in responding if hard to recall/confidential etc.

It was the 2020 return, our first. We took financial advice in Sept 2018, including the idea of “withdrawing your 25% tax-free lump sum whilst UK resident for tax purposes and then taking a lump sum of the balance once French tax resident… if, after having taken a lump sum, there is no possibility to take a further lump sum.” before we decided when and how to move. Clearly it was just advice, and I was conscious that we were responsible whatever we then did as far as the Impots were concerned.

We did not have any advice about what might have happened if we had paid HMRC tax, and then not managed to reclaim it in the same year. It did take a battle, but I researched and found we could get our French Fiscal numbers as soon as we became resident. So after that it was just a lengthy waiting game for HMRC to acknowledge the Form-France-Individuels for us both, which we managed by July 2019, after a number of phone calls and discussions with HMRC tax technicians.

We had advice about ties to the UK, and the benefits of having a short period of overseas residence before the end of the first UK tax year. The time taken to get a UK refund before making a french tax return might be a consideration too.

To briefly recap, I drew down @£2,500 last month to try and prompt HMRC into issuing me with a cumulative PAYE code, ahead of taking about £35,000 this month. The aim was to avoid (excessive) emergency code rates.

Best laid plans and all that. HMRC in their infinite wisdom decided to issue me with a special ‘T code’, fixing the amount of personal allowance at £500, for some unknown reason, and that requires their active involvement to change (ie is not automatically overridden by a cumulative code). I paid a bit less tax than would have been the case with the emergency code, but rather more than if I’d had a proper cumulative code.

I might be able to ‘cure’ this by ringing them up and asking for a proper cumulative code. I then take a nominal withdrawal early next calendar year, which is still in the same current UK tax year. That should sort out (ie correct) the slightly baffling code they’ve used.

All this is ultimately just cash flow, as they’ll have to refund 100% of the PAYE following the usual tax treaty claim, but there will of course be the usual 12 month + delay, knowing my luck…

I’d be very interested to hear what they say is their reasoning for giving you that T code after you ring them up.

It looks like the default amount (20%) which any pension provider is required to withhold from drawdowns as soon as more than the 25% tax free is taken from a fund. A normal UK resident is then expected to claim back any overpayment. The claim back can be submitted immediately, or, practically, for UK residents, in their annual tax return. Or if the withheld 20% is less than the % tax that turns out to be due thanks to their overall taxable income level/ tax band being higher, then in the person’s annual return declaration then extra money in addition to the 20% already withheld would be due to be paid to HMRC.

So they’ve kinda done the right thing as this fund is now on the ordinary standard 20% tax rate withholding level, ie future withdrawals will not be subject to emergency tax (at the nasty 12month rate which is what makes the emergemcy tax take really nssty). But withdrawals will be subject to 20% withholding tax as per usual as soon as 25%+ has been taken. Well, that is what it looks like.

As a UK resident, if you owed less than 20% (ie 0% to < 20%) tax on the withdrawal I think you now fill out 1 of about 3 variants of a particular HMRC form (ISTR one variant is for non residents) to recover the tax overpaid and you can do this immediately the money has been withheld. ISTR I saw somewhere the overpaid money, assuming 20% is withheld from a withdrawal by your provider using that code, comes back in 2 - 4 months.

The bit I don’t understand is are you (or perhaps this pension pot) still required to have 20% deducted by your provider and go through this rigmarole when presumably yoi’ve slready lodged rverything necessary (France Individual Form?) for HMRC to know that you’re not taxable in the UK.

PS The above is what it looks like could be going on to me, I’m not close enough to the nuts and bolts. It’s just that I’ve never heard of a T code (except maybe as "Temporary?). So I’m wondering is that a Temporary code assigned to you personally while they process some other stuff you’ve submitted or do they use T codes to link to a pension pot rather than a person

@George1 Thanks for the update George, I hope you’re recovering OK.

I too have a little update (been phoning my pension providers)- which also feeds into @KarenLot 's ideas on smaller pots. Academic for you I appreciate. Edit - I looked up what a T code is - T indicates allowances are split between 2 or more incomes and HMRC will review the code every year." Which begs the question what your other income is - presumably also with a T code…

My update -

For the large pension which will take me into France’s wealth tax bracket on full single withdrawal, the provider confirmed they won’t split it into two smaller pots and I can only make a full single transfer out - no partial transfer .

However googling this I saw someone post they had made one transfer from this provider to Hargreaves Landsdown (?) who did allow partial transfer and then a partial transfer to ii. I’d be interested if anyone has done this (e.g. to benefit from the UK’s 85K deposit protection).

Karen, I recall you mentioned some provider allowed one to have several pots too?

And on your P45 idea, both providers I spoke with said they would not take any P45’s on a full withdrawal - it would always be emergency tax applied. C’est la vie.

Hargreaves said they could take a transfer with the instruction given upfront to create 3 ‘small pots’ using the small pots regime. 3 as the max small pots anyone can access in a lifetime is 3, each being a max of £10k to get the taxfree withdrawals. So 3 per person and up to £60k sheltered for a couple.

I didn’t get the impression pots created specifically using the small pots regime attract emergency tax when accessed and unsure whether the standard tax rate (currently 20%) must be withheld by the provider but my impression was not. You do of course have to withdraw the totality of each small pot in one swoop though.

And if a pot has less than £10k in it tough you can’t make up the rest of your possible small pots tax exempt amount of £30k by creating any more pots beyond 3 in your life none over £10k.

This would have been 2 years ago, I don’t think the rules have changed since but of course any providee can decide if they are willing to do the admin for small pots. Many aren’t willing such as Vanguard.

You do pay Hargreaves a % on the transfer in but I thought it was fair to have their expertise and good communication etc

I’m sure others do it but I didn’t need to search and compared to other providers my gut feeling is yes you pay a bit but others so much worse.

Also worth mentioning I found this out whilst approaching them on behalf of a UK resident. I have no idea if govt rules or provider policies would differ if someone wasn’t resident

EDIT of course after arranging for the first £30k of the incoming transfer to go across 3 small pots you could leave the rest up to FSCS guarantee amount there then transfer excess onwards to another provider such as ii etc. Just a pity that your current provider won’t split your transfer out because you’d be subject to incoming fees for the initial transfer also for the part you’d then onward transfer elsewhere if you’re worried about the FSCS guarantee level being breached.

Many thanks for reminding me. Though of course for me I just want to split the 200K pot into two, say 150 + 50 which would avoid the 250K euro wealth tax band.

Sounds like Hargreaves could come to the rescue when the time comes! I shall sound them out.

And I think I mentioned for the purposes of the prelevement forfeiture (7.5%) rate I already discussed with the tax inspector who confirmed two pots with one provider are separate pots for lump sum withdrawal.

Brief update. (Background There’s been previous discussion about taking a small first withdrawal from a UK pension scheme, which should suffer tax at emergency rates, but which should then automatically trigger a cumulative PAYE code from HMRC. Subsequent withdrawals should be made at that - greatly reduced - withholding rate, pending ultimate HMRC agreement to refund all UK tax, following the submission of tax treaty Form France Individual.)

I withdrew a nominal £500 in late October. Some 30 working days later, I have finally received a cumulative PAYE code and an automatic refund of tax overwithheld due to the earlier emergency PAYE code. I think the advice to do this ‘two stage withdrawal’ generally works, and I’d certainly do it again for future pensions. However in my case HMRC initially issued the wrong, totally ineffective PAYE code, and the pension provider prematurely processed the relevant withdrawal, without having used the cumulative PAYE code. It necessitated two lengthy phone calls to HMRC and an additional withdrawal to get to the right answer…in the end.