Although the tax return season is (mercifully!) a long time off, I thought, given the time of year, it might be helpful to share an average exchange rate figure for £/€ for 2025, for future reference. As in previous years I have taken the closing European Central Bank (ECB) rates on 31 December 2024 and 31 December 2025. This methodology is “tolerated” (their words) by the Impôts for converting regular , recurring non Euro income to €. It is also recommended by The Connexion in its respected annual tax guide. Other types of averages (eg including using 1 January to 1 January rates, or month end averages are equally valid) may produce slightly different figures.

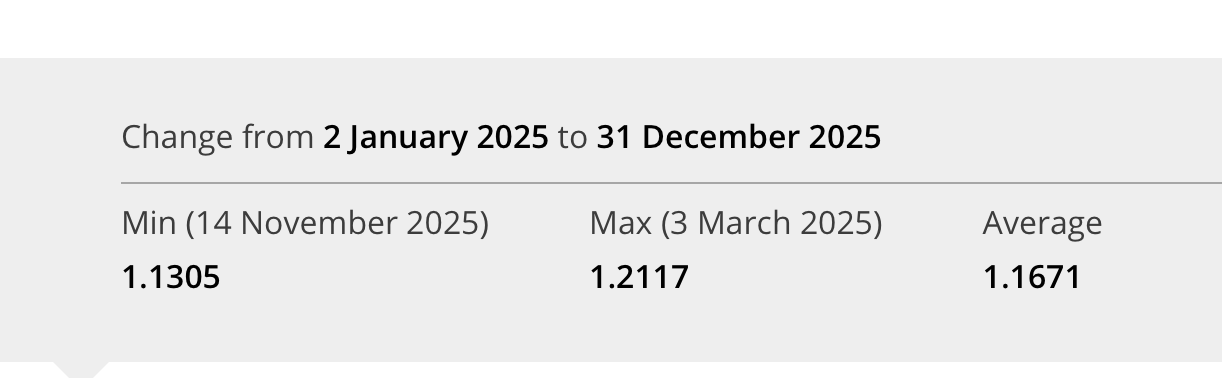

At 31.12 .24 £ was €1.2059

At 31.12 25 £ was €1.146

Average therefore is €1.176, (being a 5% decline in £’s value during the year…)

FYI the above rates are the official ECB € foreign exchange figures, which various Euro country central banks - like the Banque de France - effectively simply copy and place on their own websites. BdF, like other Euro member state central banks, by definition cannot produce its own ‘independent’ exchange rates…

You have beaten me to it George, - but it is still bank holidays in Scotland! You’ve saved me that calculation.

Interestingly for me, putting that number into the France tax 2025 spreadsheet, instead of the 1.15 I had channeled, results in a grand total of 73£ more on the tax bill, buying euro’s at 1.176 of course. If buying at 1.15 it’s bit more at 136£.

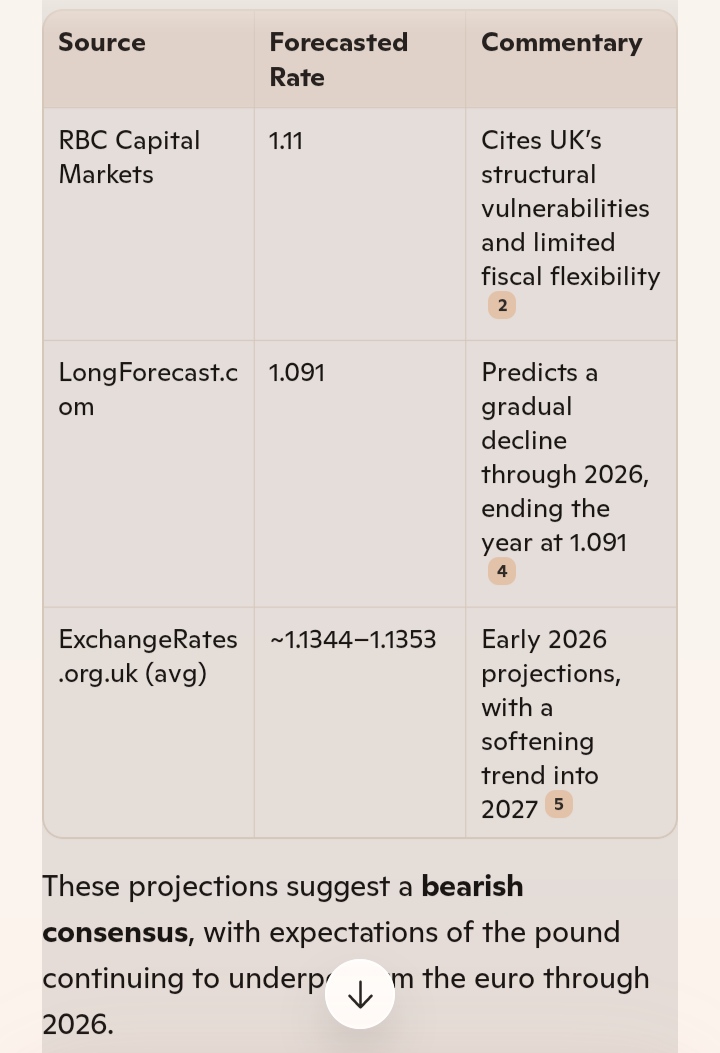

I guess the message is buy your euro’s for the tax bill now - before it carries on down to 1.12 ish? SocGen reckons 1.11 in 12 months.

..which begs the questions - why is this happening, and will it continue. AI summary below.. together with further (relatively dire!) forecasts if you’re holding £.

“Why the Pound Is Falling Against the Euro

Several key factors are contributing to the pound’s continued decline relative to the euro:

- Interest Rate Divergence: The Bank of England is signaling rate cuts in 2026, while the European Central Bank (ECB) is maintaining a more cautious stance. Lower UK rates reduce the pound’s yield appeal to investors.

- Political Instability: Ongoing leadership challenges in the UK government are undermining investor confidence, adding volatility to sterling.

- Structural Weaknesses:

The UK runs a chronic current account deficit, which makes the pound more vulnerable to external shocks.

RBC Capital Markets notes the UK’s negative net international investment position of around £280 billion, which weighs on long-term currency strength.

- Eurozone Resilience: The euro has been buoyed by modest economic growth (projected at 1.6% in 2026) and ECB policy aimed at maintaining inflation control, making it relatively stronger.”

I’ve got a brilliant idea, to avoid even more depression, while I am waiting for the rate to get better, from now on I will call all my pounds, euros, which will make me feel much richer.

I thought the official line was to use the exchange rate on the date of the transaction. It might not make much difference for small transactions, but a cash in of a policy , pension pot etc could get you in trouble with impots if they chose to look at the actual rate on the day versus a yearly average used instead

I think that, strictly, it’s the date on which we receive the original amount before transferring it. As @George1 quite rightly says, an “average” over the year is explicitly tolerated and in fact usually supplied by local impot offices. It’s not, of course, an average - it’s half-way between the beginning and end of year rates, which is no way an average over the year!

I think, and according to the Connexion, it is an accepted official policy publicly stated by whichever minister is responsible for this aspect of french taxation to use the average figure as Gearge1 has calculated. Regular income - ie pensions - isn’t going to cause tax bods too many problems. In the past, and because I’ve always completed a paper form rather than on-line, I would take a copy of the rate published by the Connexion, and include that with tax return indicating that I’d used the average accepted rate over the year. But it obviously makes a difference to large, one-off payments and common-sense tells you that it is the date that such funds arrive in france - then that is the date to use for exchange for that particular arrival of money. But don’t tie yourselves in knots over regular income payments from UK - not worth it - and the official line is the one to follow - after all, if a Minister of the Interior has decreed it is acceptable - who are we to argue !!

If you have regular income such as pensions, rent, salaries etc then using an average exchange rate for the year has for many years been either recommended, accepted, or ‘tolerated’ (depending on the Impôts office concerned). As you and others have said, for one off sums, such as lump sum pensions, sale of property etc, the position is clear - you should use the exchange rate on the date of the transaction.

When I received .my tax form from the Impôts to fill out last year, they’d already written on the first page, by hand, the exchange rate they wanted me to use.

I think this must be a general thing they are now doing as having used the rate seen on here each year previously, the rate I used had never been queried. Maybe they do it now to reduce the number of times people ask them the same question about what rate should tbey use.

I always just put down exactly how many euros we get when we transfer money from the UK to France. As that’s the actual amount of money we received, it seems to me to be the fairest method. They haven’t argued with that method so far.

Arguing slightly against myself…my UK pension is paid either directly to France (so automatically converted on the day of receipt) or is transferred by me on the day of receipt - again automatically converted then and there.

Purely out of curiosity I took my annual £ pension figure and converted it at the average exchange rate I mentioned at the top of this thread (£1:€1.176). It produced an income figure at least €1000 higher than the actual figures! There are obviously some downsides from using averages for regular income, albeit there is still a significant convenience plus factor.

In this environment of reducing GBP, it seems to make sense - and the exchange costs are taken into account.

I guess the difficulty would be if you didn’t change all your UK income received during the year, there would still have to me some method to account for that.

Precisely. For example, our UK rental income never leaves the UK. It goes into a UK bank account. Still has to be declared in France though, with an itemised list of every repair so being able to use a single average exchange rate saves a lot of hassle.

I’m in same situation - rental income; I’ve never listed separately each item of repair - just listed ‘repair’ - and then total; same for items replaced - just one total; and as it’s taxed/reported in UK then the French tax bods should accept - and have - one total for each ‘repair’ listed.