Hi, I’ve lived in France since 1996 and have worked here and paid into the French system the whole time. I’m 51 now, eligible for French pension at 64 (with children counting towards trimestres).

I’m thinking about possibly moving back the UK in the next 3-5 years.

I can’t seem to find out if I can/should maybe make some voluntary NI contributions to count towards eligibility for a UK state pension.

I think my years paying into the French system would qualify me for a state pension if I did move back anyway, but that any UK pension would be based on the actual contributions I have made. (In addition to my French pension, also on a pro-rata basis).

The thing is, I don’t think I have made any NI contributions. I did have summer jobs as a student in the UK (working for a bank) and have some paperwork somewhere, but this was back in the mid-1990s.

I know I need to contact NI/DWP, but does anyone here have any experience/thoughts on this?

I’d be really grateful for your help.

Basically, if I am able to do so, would it be worth ‘buying’ ten year’s worth of NI contributions towards the UK state pension?

Would that depend on whether I do return to the UK?

How much UK pension would I get?

Also, if I were to return to the UK and continued working there until I was 64 (age at which I would be entitled to claim my French basic and work place pension) would I be able to actually put in a claim for it, or would I have to carry on working until age 67 (or maybe even 70 by then), as my claim would have to go through the UK system, which I can only do when I reach UK retirement age?

Thanks Gareth,

The Government Gateway…I have received my number (recently inherited a property in the UK so I’m a NRL), but can’t sign up for the online thing. I didn’t have the required ID, and all the lines were busy when I called to try and sort it out. Need to get onto them tomorrow. (I LOATHE admin!).

I suppose checking my NI record is the first step.

The deadline for making additional NI contributions beyond the past six years is fast approaching but the good news is that you don’t need to have a Government Gateway account to make a payment to HMRC. This site explains pretty much everything -

Once you reach the qualifying age to claim your French pension you can do so. Your UK pension status would not be relevant i.e. claim your French one at 64 , then claim the UK one once you get to whatever is the state pension age by the time you get there.

If you can afford to just live on your French pension for a while, I understand (just hearsay) that if you defer taking your UK pension it increases year on year very nicely. No doubt there are others here who can give you more accurate info.

So did I, also I was short of some NI payments in the UK years ago, came here to work at age 57 25 years ago before retiring at 60 and got my UK pension without any bother when it was due.

Yes if you can afford to wait it goes up by 1% for every 9 weeks that you defer it by, which is 5.8% a year.

But equally you do want to look at your NI contributions and calculate whether topping those up for any missing years is worth it in order to get the full State Pension amount.

You need 35 years of contributions IIRC. I had a few years missing when I worked abroad but I didn’t need to top up as I racked up the 35 years even with those drop-out years.

I think for many people it is worth topping up, but do the maths and take advice from a professional adviser if needed.

ETA: If you want to defer your UK State Pension you don’t have to do anything - they don;t start paying you until you claim it.

I decided to take my UK State Pension when I became eligible, as the extra dosh is helpful when you are self-employed like me; I have also been able to put some of it into my private pension fund, which has gone up by 12% this year so it was worth the gamble! No doubt Trump will put a stop to that kind of gain this year though… but for me having the flexibility was worth not getting the SP bump up,

I believe you can “pause” your UK state pension once you have started taking it, in order to trigger the increase, but only once.

Also, there are issues with deferring if you are claiming state benefits; you don;t get the extra if you defer your pension in that circumstance, or if you have a partner who gets benefits.

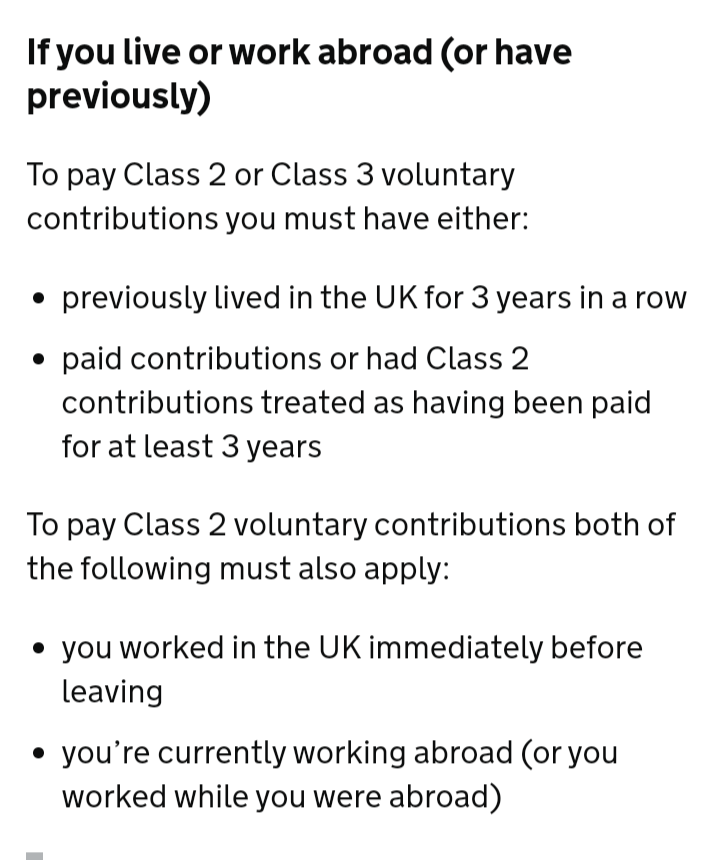

My wife bought 17 years in 2022, she was able to pay Class 2 contributions bar one year so the total cost was £3K. Complete no brainer and the payback will be less than a year if she lives to 68.

Sort of, she couldn’t top up completely because of her age but as she’s been working in the UK since 2023 she’s now has the full 35 years.

The best thing for you is to contact HMRC before the 5th of April and request a “call back” which ensures you are able to top-up from 2007 to around 2019 and buys you a little time whilst you get a Government Gateway account sorted.

This is not always the case (although everyone is told this). The OH has recently topped up three years of class 2 NI (much cheaper than class 3) and has taken his full years to 29 - This has been confirmed as his full contribution needed to receive a full UK state pension when he finally reaches the qualifying age (currently 67 for him, possibly increasing).