If you have a non French company pension paid directly to you in France, do you know what exchange rates are being used? I didn’t.

My former (UK) employer’s pension scheme pays me directly in France in euros, via its bank, for convenience and to avoid bank charges. However the exchange rates used are never disclosed to me.

On an unrelated matter, I recently came across my £ payslips, buried deep in the pension scheme portal. Out of curiosity I compared the £ pension with what I actually received in €, and was quite disappointed. I dug a bit deeper.

Over the past 8 months, they have used inferior rates to the readily available market ones, in 4/8 months. I worked out what I would have received if they’d used Wise/Xe rates. €625 is the shortfall. That becomes real money, the longer this continues.

I’ve now requested a switch to paying my pension to my UK account and I will obviously be responsible for the decision on when/at what rate it’s worthwhile transferring.

I’m sure there are probably some others who may be in a similar situation,(in which case this post might be helpful in focusing attention on the rates being used?). I suspect there are probably also lots who are acutely aware of the exchange rates being used,.and no doubt think this is all rather obvious…

A good point! I think the State Pension gives a decent rate though, fortunately.

I don’t have any occupational pensions and the private pension schemes I do have will only pay withdrawals to a UK bank account, so for me the point is moot, but I shall still be doing my currency exchanges manually!

We decided to have pensions paid to our UK accounts. Some companies won’t pay into anything else but if they do,in general, the transfers appear to be subcontracted to someone else and are poor. The State pension has been at least as good as I could do, so we’re continuing with that being paid direct to France.

Are you going to challenge them, George1? In the business they’re in, they cannot ‘not’ have known what they were doing.

I’d reconvert at Bank rate and present them with a request for a refund as well as fair Bank rate in the future. As no doubt an extremely large financial institution, they will have had access to the best FX rates available.

I know you won’t get Bank rate but that would be my opening negotiating position. Wise cost would be my lowest acceptable point but actually you shouldn’t have to settle for far off Bank Rate at all (usually istr you’d be negotiatig to 4 digits after the decimal point).

I’d frame it in a letter expressing concern to the Trustees.

If they’ve done this I’m wondering whether if you did anything else with them, could it be worth a dive into how those things were calculated too. Eg commutation rates they used for lump sums, incorrect assumptions used about things like the demographics of the mrmbership when calculating transfer values etc.

I like your style Karen! Thank you for the suggestions .I have now raised the issue with the administrators, and we’ll see what - if anything (!) - happens.

My assumption is that the administrators (Capita) will say, “nothing to do with us, we outsource all the foreign currency payments issues to our bank, Citi. Neither we, nor our bankers make any contractual guarantees of exchange rates etc”. The trustees (who will probably hear about this from the administrators) will no doubt say we outsource all that sort of thing to Capita to deal with. Citi, who are probably the ones actually profiting here, will claim they at all times use market rates to best service their valuable corporate clients etc etc.

I also think there is a personal responsibility issue here. It was my decision entirely to have my pension paid in euros (via the Single Euro Payment Area - SEPA) directly to France to avoid the tiresome, irritating bank charges that would otherwise arise through not using SEPA, and instead using SWIFT. If I’d been thinking about the issue more deeply, I could have established that the rates being used by Citi were seemingly below best market rates, at an earlier point in time, and switched to payments in £ into my UK account. As it is, I’ve had a pension in payment for less than 18 months, so at least I’ve realised in time, before amounts started to seriously rack up. I will put it down to experience. This is why I did the original post, to prompt any others in the same situation, with non French employer pensions paid to them in France, to consider taking action to mitigate the exchange costs.

If I hear anything back I will of course update the thread…I’m not holding my breath!

Given your vast and valued experience and advice freely given around taxation and pensions I think you can be forgiven for this oversight which you admit is entirely your responsibility.

Your former employer has paid your pension and like all things in life if a middle man is involved they will take their cut one way or the other.

I really wouldn’t hold your breath expecting recompense and instead be content in realising your ovrrsight sooner rather than later.

Since it is your former employer and I presume you don’t have much to lose, do they have a Facebook or some other social media page where they could perhaps be shamed into taking action?

I don’t have that option with my US pension, but I just keep invested it in the US now. We live off my US Social Security which goes into our French account in euros. Supposedly at the best exchange rate the USG can extort but everything coming from there seems to be a big lie now.

Reading that - my heart sank! I have a Unilever pension paid here in France whose administrators are Crapita (as Private Eye calls them). Has never occurred to me to query this as I understood Unilever has the buying power in the forex market to get a good exchange rate and that’s why I was happy to have my pension paid straight into my French bank account.

The frustrating thing John is that when I started this it was Unilever’s own pensions department who managed my pension. The addition of the “middle man” and the cut that this middle man takes was for the convenience of Unilever. I’m not sure my pension should now be worth less in euros because it suits Unilever to have done this - I will investigate further.

I believe (though I may be wrong) that letters addressed to the Trustees may well get auto directed to the pension administrators but there may be a smidgen more attention if addressed to Trustees.

If it was a really big issue I’d find out who is on the Trustee Board and write to an individual Trustee at their other business address, or private address if I happened to know them/it and that would guarantee attention.

In my albeit limited observation there are 2 issues with anything the pension administrator gets their hands on, first.

The biggest issue is they go into ar$e-covering mode immediately on literally anything (denial, obfuscation, lame excuses, and other general ar$e-covering). In this it is not to cover themselves from the pensioner/scheme member. It is to cover themsrlves first with the regulator, and after that, with the Trustees. The member is not even on their list as a ‘client’ really.

The other issue with things landing with the administrators first is their incompetence. Partly the level of people who will pick it up, partly, I believe, the owners of the pension administration keeping them that way for compliance reasons.

It’s quite simple, if you can afford to wait awhile if necessary, you can watch the daily rates and choose your own moment to grab a good one, from the built up pension that is sitting in your UK bank account. Of course, that assumes that you have managed to hang onto one.

I got 1.20 in March and 1.18 in May, didn’t need any at the moment so leaving it alone while it languishes around 1.15. It’s the end of the month today so they would be paying more in about now, better in pounds rather than buying euros at a lousy rate.

Yes, of course that’s the downside, literally, but at least I can chose the moment for myself, maybe now, maybe next week, but at least no more relying on others to take the decisions.

Say that forecast is correct, I can at least buy some euros now and then again in a week or two and I’ll still be better off than waiting helplessly ‘till the end of september.

It’s possible that Unilever has different foreign exchange arrangements for paying pensions with Capita than my employer. However the chances are that it’s probably similarly outsourced to a bank like Citi.

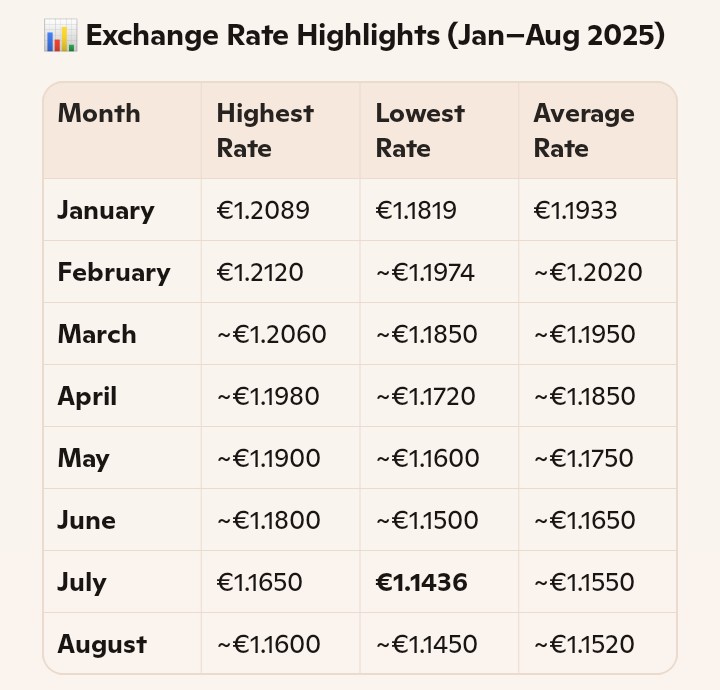

If its any help, I used this table to compare the monthly market rates they should have used, during this calendar year, against the.actual rates Citi must have used to pay me in euros, based on what appeared in my French bank account.

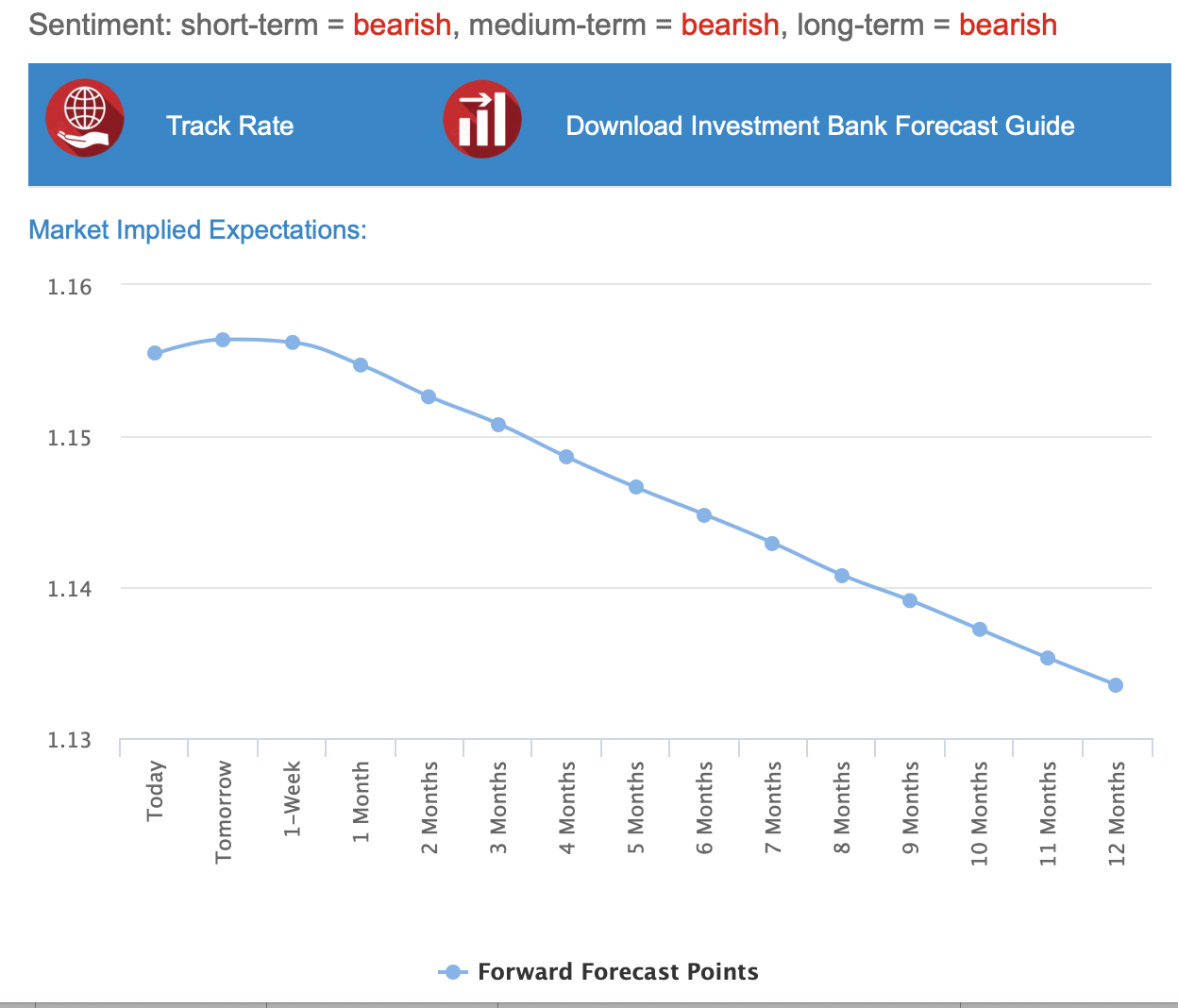

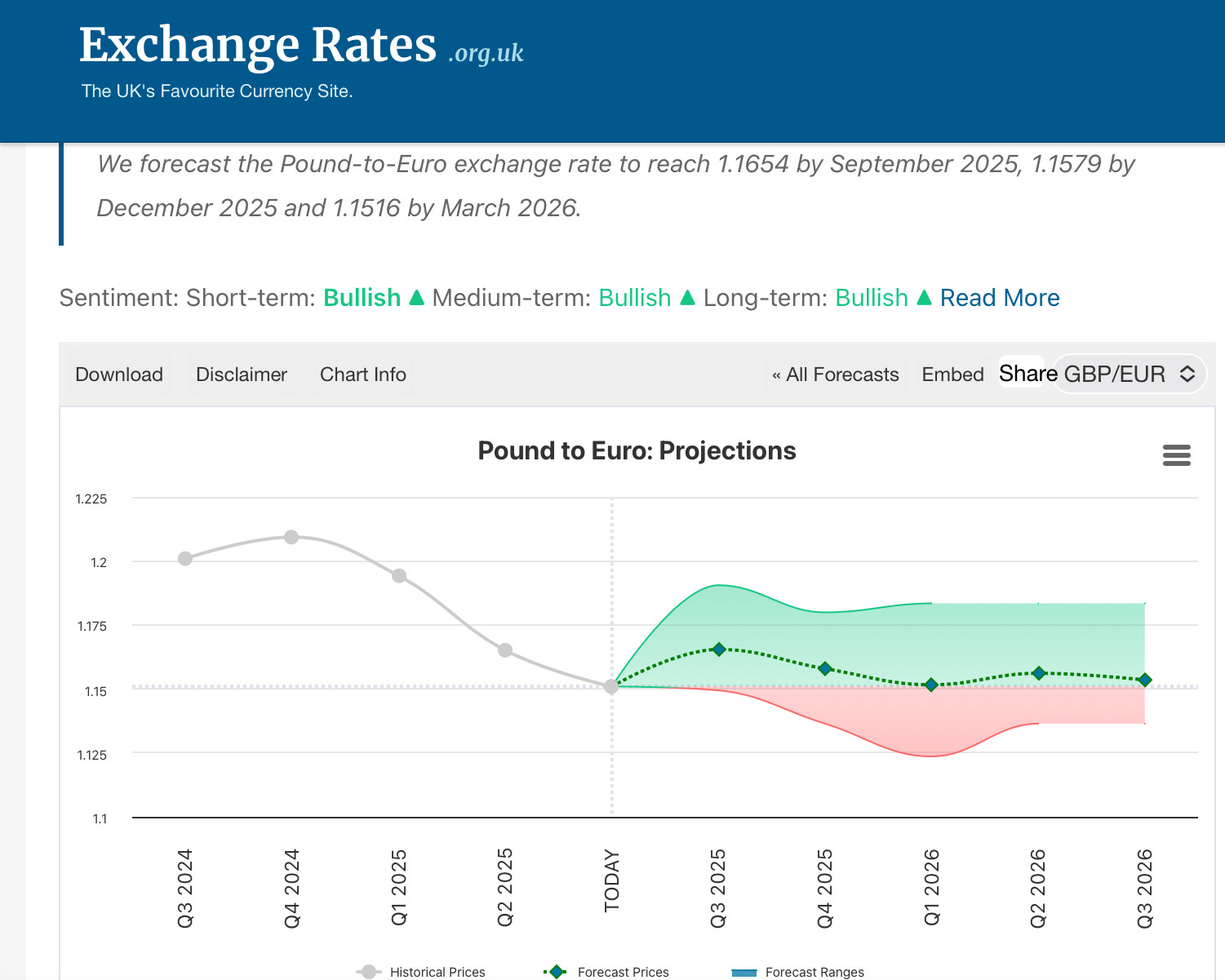

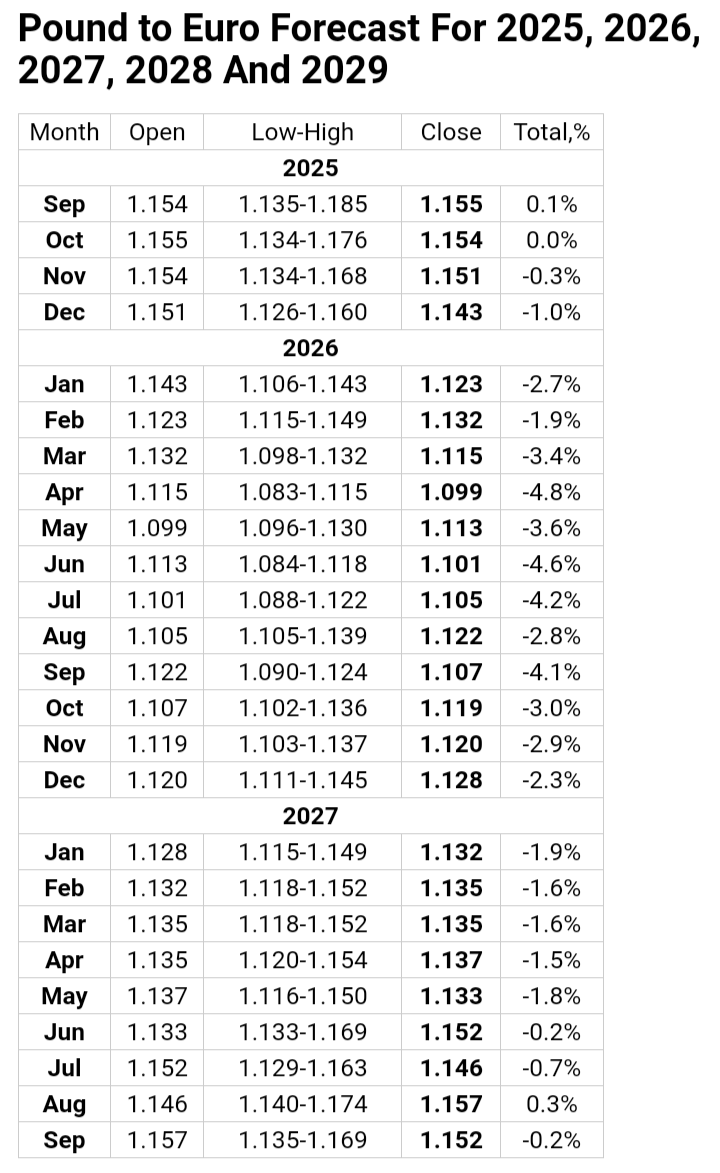

Supporting the trend identified by @larkswood12 I came across this table showing the forecast £/€ rate for the next two years. 2028 and 2029 extended beyond the screen so are not shown.. However the trend remains fairly dismal. Obviously still crystal balls…

It makes me think that building up a bank of £ in the UK, whilst waiting for a better rate to transfer to € might not be the right move for the next couple of years, and seemingly the two years beyond that.I’m thinking it may be better to transfer the monthly pensions received in £ to € shortly after receipt.

I received a legacy in US dollars. I asked my bank manager when I should transfer it. He said that if he knew that he would be very rich and not a bank manager.

I have two uk pensions paid in uk and I use Wise to transfer them. Their fees are low and they use close to the mid exchange rate