Finally I got old and I have to open the drawers from hell and start opening 10 year’s mail about pensions. Or maybe avoid that a bit longer.

UK Employers pension from my youth kicks in this year at 60. It’s not that big but it’ll help. Two options are 3k a year or 2k a year plus a lump sum. It’s sort of index linked (old final salary scheme).

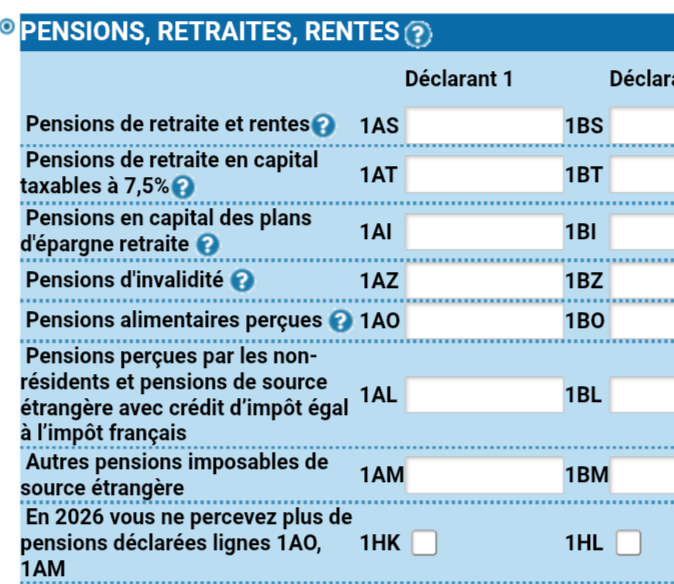

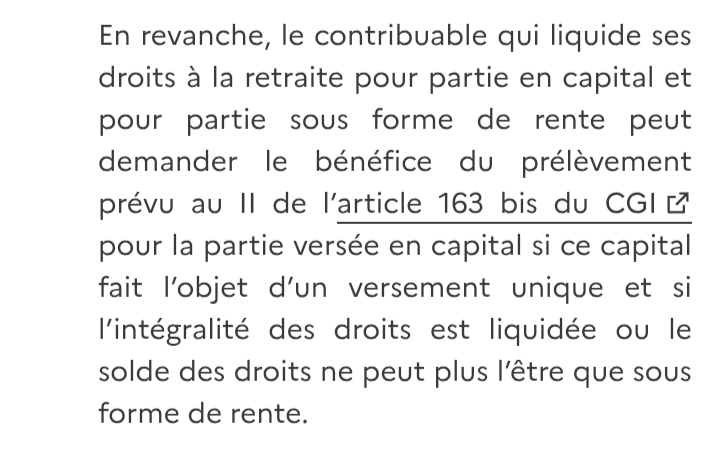

The lump sum makes more sense (it’s about 17 years worth of difference) - but it ain’t tax free in France is it?

My simple understanding is …

Standard pension goes in whatever box each year and there’s normal tax/social charges linked to total income - plus I imagine some faffing with HMRC. But fundamentally it’s income and tax is what it is.

Lump sum - no S1 - taxed/ss as a one off rather than as income (?). Plus I imagine there’ll be some drudgery with HMRC ? And obviously ongoing yearly declaration etc

Got a few months to decide. Just working out the tax bit.

Also

Does what I do with this “employer” pension affect what I can do with two small private UK pensions (neither amounts to much) be it now or 5 years down the track - in terms of lump sums.