Driving to England early next month for daughter’s wedding. I checked with my french AXA insurance provider that my fully comp insurance will be valid in UK after Brexit. I was told it would only cover 3rd party.

Anyone else had the same experience? AXA are a multinational organisation, why can’t they manage this?

I have looked for breakdown cover for a French car whilst in the UK for approx 10 days, can not find anything, however, plenty for UK people bringing their vehicles to EU but nothing the other way.

Is this another Brexit benefit…?

Isn’t this a very common issue? I’m more familiar with it the other way round in years gone by when I had a UK insured car, that lost the fully comp when I crossed the channel. So not sure it has anything to do with Brexit (for once!).

Don’t go to UK with a car much, but last time just spoke to my insurer broker who added fully comp on for a few €.

Have a lovely wedding

(Une assistance-dépannage pour sa voiture hors Europe est une demande très particulière. Il vaut mieux contacter directement une assurance spécialisée, son propre assureur ou un courtier pour ce type de couverture.)

As Jane says it’s pretty much the norm for UK policies to only include the minimum cover which is legally necessary when driving abroad.

And, yes, you can add a week for maybe £30 or so - but that gets quite expensive when making several trips a year. Plus, the one time that you forget will be the time that something happens.

None of which bothers me as much as the fact that it seems to be so opaque in the UK - the policy will say “includes European cover” but not at what level and even if you phone customer support you seem to get some clueless operator who suddenly doesn’t seem to grasp the difference between 3rd party only and fully comprehensive. I’ve resorted to asking “so, if I skid and hit a tree am I covered” - “oh, er I’ll check, no, sorry”.

I’m with Aviva at the moment - they say the policy is “completely the same” as when I’m driving in the UK - hoping not to need to put that claim to the test.

This is the first time I have heard this, and is very disturbing bearing in mind my frequent criss crossing of The Channel over many years with dogs, as well as family visits.

I’m with AXA too, so will be asking the question very soon, altough I have no plans to ever make the trip again.

ADAC do breakdown cover in the EU which us living in the UK cannot get now because of Brexit. Might be worth a call?

I selected my cover in the UK on the basis it did provide the same as the UK cover fully comprehensive, funny how that means less than fully comprehensive to an insurer! So in a weired way AXA UK does give fully comp in the EU. However AXA also owns Swiftcover that does not, devil is always in the detail with insurers.

I am not with AXA or Swiftcover, prefering a mutual where I can.

I had that a few years ago and, when I came to use it, it was awful. They got my bike back to the ferry and left me to it, so ended up riding back to Wiltshire with no clutch cable. There was quite a low limit on the recovery cost that they would pay and it was just enough to get me to Calais.

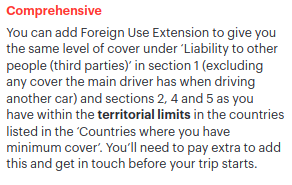

I’m surprised to hear that, as far as I am aware my policies have always included comprehensive cover in the EU - here’s what the current one says:

When you are driving in the Channel Islands, the Isle of Man, Iceland, Norway, Switzerland, Liechtenstein, Andorra, Monaco, San Marino, Gibraltar or Serbia and any country that is a member of the European Union, you’ll have the same level of cover as you have in the UK, for up to 90 days per trip. We will only provide this cover if your permanent home is in the UK and your visit abroad is temporary.

It does however say that “Cover for driving other cars is restricted to the UK”.

Similarly my motorcycle insurance makes no mention of reduced cover when riding outside the UK, though it does say “You must notify your insurance intermediary of the details of any journey outside of the UK prior to travelling.” which is some small print I haven’t seen before. I will be checking that one with them before I whizz over next month.

That said I never go for the absolute cheapest cover available, so maybe budget policies will limit cover outside the UK?

On a general note, insurance companies are barstewards and will be first up against the wall when the revolution comes.

Sometime (best done over a beer or other alcoholic beverage) I shall relate the long and tedious saga of what happened when I was a student and I had my motorcycle stolen, then borrowed a friend’s bike and got knocked off that one by a blind motorist… Suffice it to say it took a year to sort out a very simple claim.

A couple of years back I had a somewhat expensive car nicked. Needless to say the initial offer was rather less than I paid for the car - and woefully under what it would have taken to replace it (I never found the same colour/spec) because I had nabbed something of a bargain when the market was very sluggish because of Covid and by a year later the like for like price was about 30% (and several thousand £) higher.

In retrospect I think I picked up an ex-demonstrator given the very low mileage, extensive options and low price, plus the fact that an engine mount broke shortly after I bought it which really shouldn’t happen with expensive German cars.

In the end I got them up to the purchase price but that was as high as they would go.

To be fair this means that I have “won” the insurance game - they paid out more than I ever paid them in premiums. In fact I think even if I insure expensive cars for the next 20 years I’ll be up on the deal.

But the learned lesson was that the insurer does not count the price of options, nor expensive colour options when figuring out what to pay you - they just value the basic car, which is why there is a market for “gap” insurance (i.e one rip off on top of another).

This is very interesting @David_Spardo and, like @Epagne , I shall be interested to know what you find out!. I haven’t been to the UK for several years now but, given that I have a new (to me) car and may have to do a trip later in the year, I would be most concerned if I was only covered 3rd party. I’m fairly sure that I’m covered for breakdown though…

Covered for breakdown - in the UK? I would check if I were you.

AXA offices appear to be run as franchise operations in France, I wonder whether the extent of insurance cover may vary from bureau to bureau.

I was going to slag AXA UK off over this but looking at their policy documents in detail I think you might be OK in the EU if you have a UK AXA policy.

Pacifica rather than AXA in our case…When I took out cover last week for a ‘new’ (to us) second hand car, Pacifica specifically confirmed cover outside France is exactly the same as for our fully comprehensive cover in France, provided no journey is more than 90 days. The only exceptions to the coverage rule are for visits to Russia, Belarus and Iran (I guess I’ll now have to change my holiday plans!).