IMO Hunt, he who cannot remember his wife’s nationality, is the cause of the junior doctor’s pay issues. He clobbered them during his time as Health Secretary (2012-2018) yet nobody is chasing him about it. The ability of politicians to do damage and then, in the twinkling of an eye, move on is a big issue for me. What’s the motivation to get things right if you can just airbrush your disasters out of your history? They should all be dragging their track records around with them like a ball and chain not skipping from one cock-up to the next.

Once a Hunt, always a Hunt

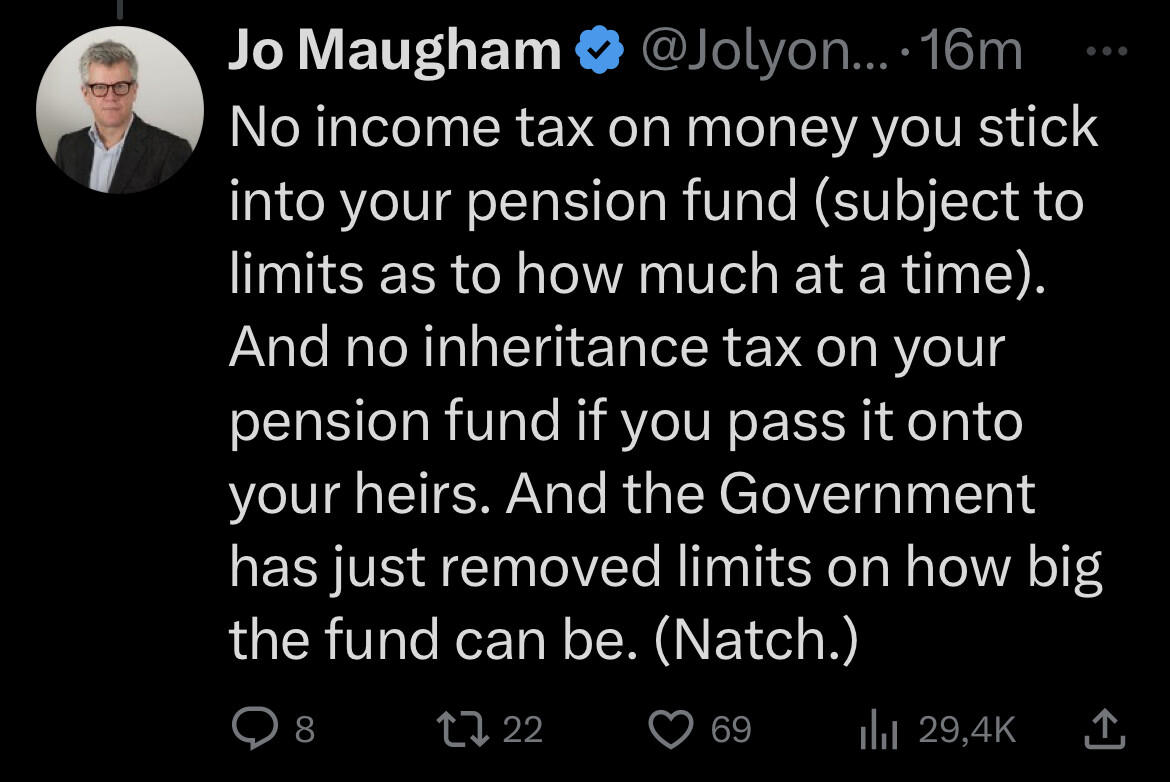

His budget today is a farce… no money for Junior doctors and others but he can manage to remove entirely the lifetime limit on pensions so if his super-rich friends (and no doubt party donors) can find a spare £billion or so down the back of the sofa to stuff in to their pension pots they won’t be taxed on it

despicable moron.

Yes, but I was listening to this guy on PM John Glen (politician) - Wikipedia he’s very smooth. Does a good “the acceptable face of compassionate conservatism” act. Don’t want too many of him around pulling the wool over people’s eyes again

I can’t ever remember bursting out laughing before when listening to a Budget Statement. Why did we ever leave the land of milk and honey that is the UK?

Starmer had it right “the sick man of Europe once again”.

Another appalling trade deal post Brexit.

Malaysia has been allowed access to UK for its palm oil just so that the Tory government can say they have made another good deal post Brexit.

Hopefully Brits will not buy their goods containing this palm oil.

Actually abolishing the LTA, as well as benefiting the usual suspects, is going to benefit senior doctors. The ones who earn over about £200,000 p.a. apparently.

The Tory story (and probably the story of the BMA aka the doctors’ union) was that too many of these very senior doctors were retiring /leaving the NHS / refusing to work extra hours because they were losing money due to being taxed if they continued working. At a great loss to.the NHS etc…

I’m guessing these highly paid public service fatcats’ Defined Benefit pensions had breached the LTA. So no more pension benefit could be attributed to them in their Defined Benefit scheme without them having to pay tax on that accruing benefit, out of current earnings. Thus it looked like it was costing them money (but was only asking them to pay a slice of tax on a highly valuable increase in benefit attributed to them within the pension fund… which they were old enough to be able to access quite soon including a possible monster lump of taxfree cash.)

That’s roughly what it feels like having watched this [lobbying by the BMA] covered very frequently in the financial UK press over the past three years.

And don’t get me started on why ordinary workers whose employers gave up being able to afford to provide them extremely expensive Defined Benefit pensions 2 decades ago or more, are still having to fund public service Defined Benefit indexed (inflation-protected) pensions through their taxes when they can’t afford them for themselves.

Public service pensions are ‘unfunded’ (ie there’s no money behind them the pensions are all paid by taxpayers),. Whereas private sector workers who are paying for this don’t get this type of pension themselves anymore due to its unaffordability for employers and themselves. And yet this unfairness is not being addressed.

The old rough rule of thumb used to be that for a pension of X you needed 20X in your pension pot. So you could salt away sufficient for a 100K pension in your private pension before hitting the cap. If you’re a doctor in the NHS then you’re part of the NHS pension scheme so there must be some way the value of a individual’s “pot” is imputed to see if it’s over 2M. I wonder what the factor are (were).

As I understand it after overhearing OH’s R4, it’s ostensibly to encourage NHS doctors to stay on beyond 55 years old, which is the age at which apparently many currently hit the pension tax threshold. However, whether or not this is the case and if so, whether or not it would work, I haven’t a clue (and I suspect very few have either).

Yes, it’s about 20 multiplier for DB too. But the problem with Defined Benefit pensions is that as they’re such high value pensions compared to what people paying into today’s riskier lower-returning pensions can afford to pay (eg SIPPS and other Defined Contribution pensions), people with Defined Benefit pensions have been particularly prone to being told that the value of the amount nominally held in their Defined Benefit pension scheme needed to fund their pension, had breached the LTA.

This meant that they would have to pay a % of tax on the value of further credits into the Defined Benefit scheme on their behalf each year. So they could have accrued a nominal £1.8m (ie reached the value of the LTA), at age 55 say, and every year after that they worked, more would be ‘booked’ to them in their Defined Benefit scheme, so they’d be taxed as though they had received that value as income each year. As having reached the LTA, pension contributions or credits made by them or for them, were no longer tax free.

Many of these DB schemes being non-contributory, so they hadn’t actually had to pay for it, being charged the tax out of the monthly pay packet for breaching the LTA, felt like a pay cut. As they lost cash, even though they were accruing a considerably larger benefit in the pension scheme that they could access shortly or even immediately (though due to something called the MPAA, immediately would be unwise, if still working).

Don’t forget that if the amount is £1.1 million or so upwards in a scheme, perhaps a bit more in a defined benefit scheme, then at any time after age 55 (soon to be 57), 25% of it can be taken out tax free as a lump sum up to £268,000. So long as not one Penny more than 25% was taken, they could get that taxfree, and continue working and contributing up to a new £40,000 (soon to be £60,000 since yesterday) back into their pension each year.

If you’re over 75, I think, at your departure, I think pensions can be bequeathed tax free.

Pensions have held up against various tax attacks of desperate Chancellors (such as the halving of the capital gains tax exemption threshold this coming 6th April). Looks like 2 years before the next election, the Tories have opened the floodgates for those needing to shelter funds.

I guess the working person on an average salary will have to wait until next year, close enough to the general election (as the plebs live hand to mouth so might forget if anything were done for them other than right before the election), whereas the wealthy can plan over longer time spans.