I may be wrong, but I think that is the point. It is one thing to move to France and change to a French address with an existing UK bank a/c. OH and I have between us HSBC, First Direct and Nat West a/cs all with French addresses. BUT they were all set up many years ago. As JohnBoy says:

At the time we thought Barclaycard were going to close our credit card a/cs because we are living in France (they didn’t) we explored alternative solutions for taking up a UK credit card with another UK provider. We did not find any who would take on a new relationship outside the UK.

Brick and Mortar Banks generally do not provide a good exchange rate - this has been done to death on SF.

Better to use a Fincon like Revolut, Wise and others - TorFX for larger amounts are usually better too.

I think that is also the point here… to try and do that now since Brexit may be difficult (as the Topic outlines) and that account facility could well be at risk of withdrawal at any time. As @JohnBoy so rightly posts:

Why am I hoodwinking them? I have a house in the UK and a house in France. As I said, Lloyds have known for 20+years and know I am tax resident in France. I’ve had Lloyds accounts since the mid-1970s. I’ll leave it to Lloyds to decide whether they want to let me retain the account.

If you move outside the UK in the future, you must let us know. Most customers will be able to continue to hold their UK banking product. For customers living in certain EU countries, however, we will not be able to provide some UK banking products and services after 31st December 2020. We have contacted customers whose accounts or services are impacted by this.

but I guess your residence in France is your primary residence, no?

As for HSBC, I’ve been looking further into your suggestion.

There’s a lot of faffing about to be honest and the are are aspects which are unachievable… in particular -

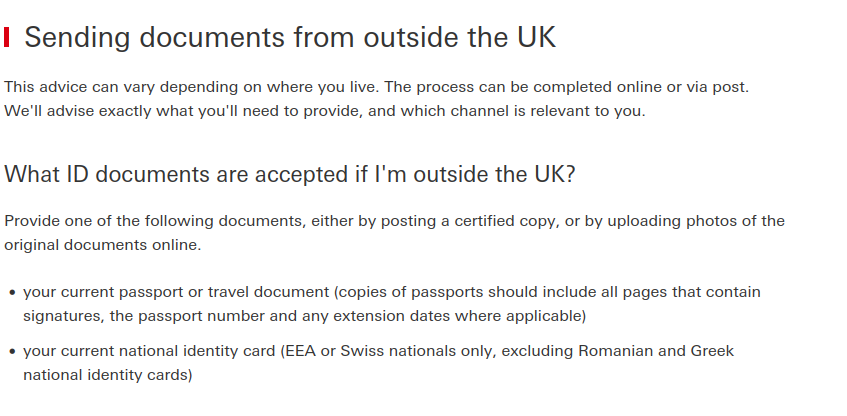

Most UK residents in France cannot produce a current National identity card - only a residents permit (CdS) and this condition (to produce an ID card) appears to apply to those with nationality…

My reference to this is here from the HSBC website itself. I doubt many people would even bother to be honest, I certainly wouldn’t… life is too short and why jump through these hoops in the first place when in reality, it is so unnecessary.

I really don’t know why I’m bothering with this. Yes, Lloyds know my French address is my primary residence. The accounts were changed to the French address when I moved. Later, when querying something in a UK branch it was suggested I could change the account address to my UK address (I think because it gave them the opportunity to sell financial products).

But, as I quoted from the Lloyd web site above, Most customers will be able to continue to hold their UK banking product. For customers living in certain EU countries, however, we will not be able to provide some UK banking products and services after 31st December 2020. We have contacted customers whose accounts or services are impacted by this. it doesn’t matter.

If you read the text in full it says “Provide one of the following documents” and one of the options is:

your current passport or travel document (copies of passports should include all pages that contain signatures, the passport number and any extension dates where applicable)

Doesn‘t matter. As long as the UK bank knows that we have our primary and fiscal residence in France, and has our French tax numbers, ours are perfectly happy to keep our accounts open knowing we also have UK address and UK tax number. The issue for them is transparency and traceability of funds.

However what they won’t do is give us any advice whatsoever - but since we’ve never asked them for any this isn’t much of an issue

Is it not the case that any account from any provider in the UK is at some risk of similar action and as @JohnBoy suggests, it is better to make provisions for when that day arrives?

We did, and when Barclays pulled the plug, it was no big deal. We have similar provisions in place for when (if) Halifax do the same with our only remaining legacy UK bank account.

Did some business with HSBC recently which required me sending copies of passport, proof of address, bank account details to them on line using their security protocols. Explained here Secure email communications | HSBC Holdings plc.

No faffing about involved just professional and secure communications.

This is my thoughts too.

I think talking about what is acceptable to “UK banks” is not useful because each bank is setting its own policy and that is what customers have to comply with.

Some will be jumping through the hoops and obtaining the necessary EU banking licenses in order to be able to continue providing a full range of services to EU residents, some will provide a more limited range of services and some will decide it is not worth it and they will no longer service EU residents.

As a UK tax payer, a UK citizen and with a UK address, I wonder how a bank could refuse me? Not give advice, sure, as that needs passporting licence. But just having the account is a pretty passive thing requiring no EU permissions.

And capital gains on second home means unlikely to get rid of the address until have spent everything else - which hopefully is far in the future.

Well I’m not panicking, nor have I ignored the warning signs. There were similar issues when we moved residency from Switzerland to France, so I have been through the process before. We have been fully aware that the account could be closed, but not definitively told it would be. Why go through all the hassle of changing banks before you need to when there is no guarantee that the new bank won’t close the account at some point in the future?

Couldn’t agree more. The hassle l went through was to open a new account last year with a new bank (HSBC) not to change banks but to have a new account in place should my current bank (Barclays) decide to close, which they now have.

Yes HSBC might do the same in the future but as there seems to be no other bricks and mortar UK bank that will open an account to a new non UK resident l shall cross that bridge if needs be.