Has anyone had experience opening PEA with Britline? Is it worth doing, or would it be best to open it with Boursobank, Fortuneo, Trade Republic, etc.? I’m specifically looking into their Invest Store Intégrale options, which seem better than what other banks are offering. I’m concerned about possible hidden fees, so I’d appreciate it if you shared your experiences.

Yes, I have a PEA opened through Britline, albeit its management is presumably delegated (despite any branding) to CAs wealth management subsidiary, Indo Suez. The latter have a mixed reputation with me. Their Assurance vie performance over a number of years is mediocre, unfortunately.Their PEA performance is much better, but that is also a function of investing in a few,(about 25) real companies shares, (with France’s luxury goods companies boosting the PEA performance).

If I was starting out now, I would be looking at a PEA through a Fintech, not a bricks and mortar bank, as the latters costs - seemingly across the board in France - are high, and there is often little correlation with high costs and enhanced performance, unfortunately. Fintechs charges just have to be lower, you’d imagine (and I use them also for assurance vie, - very satisfied - as well as bricks and mortar banks).

That’s a good point, although as I mentioned above, our PEAs are amongst the better performers of our investments, so I’m inclined to leave them as is, with Indo Suez/CA. All I was trying to say above was that with the benefit of hindsight I would probably have been better off investing through Fintechs eg for PEAs, at the outset. I now only make future investments through them.

A Plan d’épargne en actions (or PEA) is a French tax favoured investment wrapper. You can only have one PEA per person and are limited to a maximum investment of €150000. After holding a PEA for 5 years, gains are free of income tax but not social charges (17.2%).

Do you have an Invest Store Intégrale with them or Invest Store Initial?

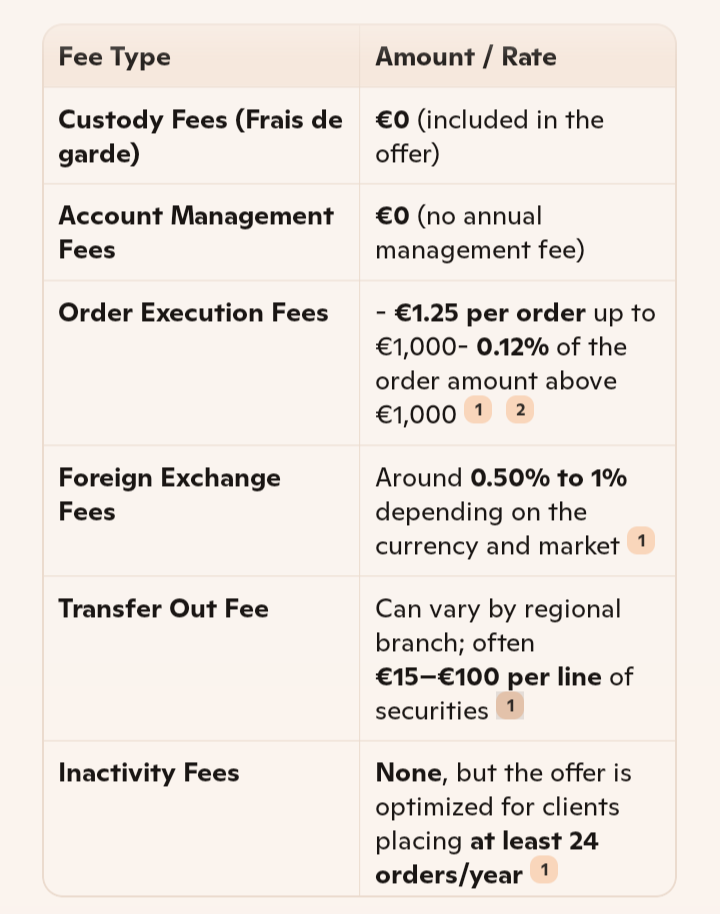

Intégrale seems to beat the offers of the neobanks, but I’m wary of hidden fees

I must admit I’d not come across either of those products (Invest Store Intégrale or Invest Store Initial), which puzzled me. I then realised that both are for investors wishing to invest/trade directly themselves. By contrast , our PEAs are managed by Indo Suez. They make all the investment decisions based on the chosen strategy by the Investor. I do not pretend to have the knowledge to make investment decisions, and in particular the allocation or weighting to individual investments so I have always used managed investment services - which obviously comes with a higher cost.

So no Capital Gains Tax ? Wondering even if no income tax, are they still taken into account within total income so that other income might then be taxed at a higher rate due to a total income threshold having been reached.

Also wondering if these social charges are affected by an S1.

Last wondering is, if the money is left for 5 years then not all taken out but just some, is there a way to consider a part withdrawal as a return of capital and not income or taxable capital gains, with the aim of leaving any amount in excess of the original sum invested till last so as to be taxed on it later.

On a partial withdrawal it will be regarded as comprising a mixture, being part a return of capital (not taxed) and part being gain (social charges only).No scope for arguing either LIFO (last in first out ) or FIFO (first in first out) basis..

It’s important to realise that you can only invest in stocks and shares, or managed funds and ETFs investing in them, in a PEA. You can have cash in there, but without interest (I believe Saxo pays interest, but not much). At our age it’s not advisable to have more than 50% of your money, at the most, in there.