We live and are taxed in France. OH has a small old UK Pru pension he wants to cash in. Can he put it straight into a Livret A ?

I don’t know but what I do know is that if he does and he dies before you, it will be locked and unavailble to you until his kids’ (if you don’t share them) inheritance is sorted out, which could take up to 10 years apparently.

1 Like

Good luck, they’re one of the worst organisations to deal with. Utterly incompetent.

1 Like

Yes, assuming he doesn’t exceed the maximum that can be contributed to a Livret A, (€22950). However the pension provider will deduct UK tax, which he will have to reclaim via Form France Individual, even though France has sole ultimate rights to tax the pension. There are several threads on SF describing how to go about making the reclaim, which is a potentially long, tedious process, that could take up to a year.

The entire amount of the pension will be taxable in France, irrespective of the fact that the UK is holding onto a percentage of it. If he takes it as a 100% lump sum, there is a favourable French tax rate of 6.75%, plus social charges if he doesn’t have a form S1.

EDIT - to reflect confirmation of Livret A threshold amount, and removal of phrase ‘emergency rates’-see below

Ooh, I missed that.

1 Like

I’m not keen on the interest rate but my wife has a serious aversion to stock market investment after her father was seriously stung in 2008.

That passed me by too, which is odd.

I just checked my bank, the service publique site & droit-finances & neither mention this change, but your linked to site seems very certain.

#confused

Yep, mine still shows €22950 as the limit and I can’t add more.

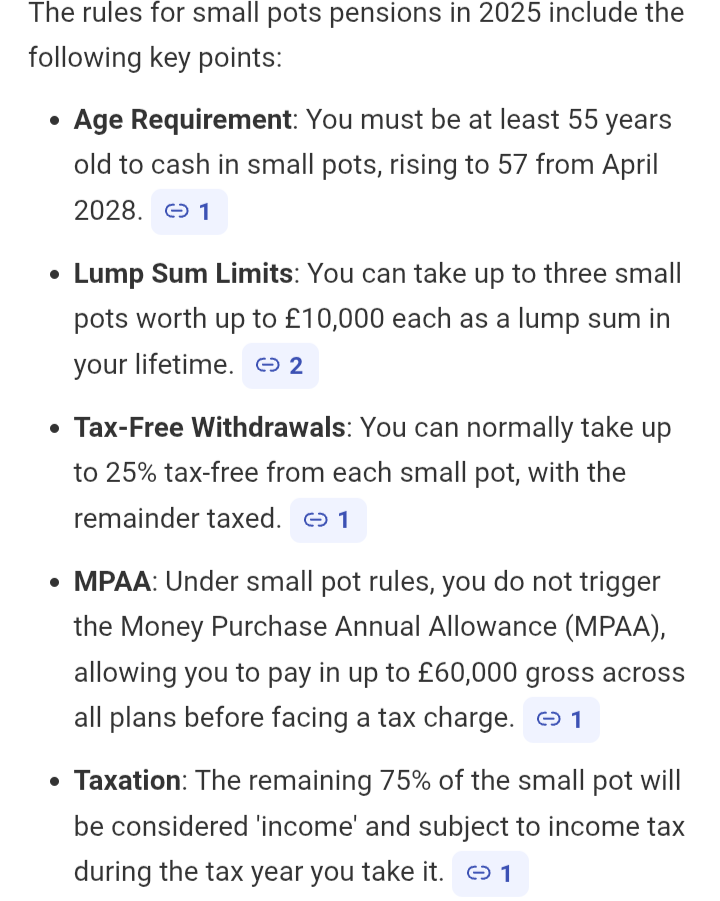

Would that apply if it’s a small pot pension<£10k?

Thank you for flagging this up (and to @JohnH). I had checked 4 articles on the subject, before posting. All were dated prior to the article I posted, so I naturally assumed that there had been a subsequent increase in the Livret A threshold, (especially as there had been media speculation of an imminent increase).. However, it now seems clear that despite the ‘certainty’.of the linked article, it is unfortunately inaccurate. Apologies for inadvertently confusing matters. I will edit the advice to @Pamela_Shields for clarity.

However this is where it gets interesting. I interrogated a couple of local AI bots to ask why there are articles claiming an increase in the Livret A thresholds. This is what one of them said (lightly edited for clarity and concision);-

“There is no official evidence of a Livret A ceiling increase as of 1 October 2025 because, although widely reported in the media, the French government has not yet published the corresponding decree or updated official channels like Service-Public.fr.

Here’s what’s going on. Media outlets such as Inspire France and Bulletin des Communes have stated that the Livret A ceiling will rise from €22,950 to €37,000 starting 1 October 2025.

What’s Missing. No decree has been published in the Journal Officiel de la République Française (JORF), which is the legal requirement for such a change to take effect. Service-Public.fr, the official government portal, has not updated its Livret A page to reflect any new ceiling. Bercy (Ministry of the Economy and Finance) has not issued a formal press release confirming the change.

Why the Discrepancy? The media reports may be based on leaks or early drafts of a decree that has not yet been finalized or promulgated. It’s possible the measure is delayed, under review, or politically sensitive, especially given the concurrent drop in Livret A interest rates from 3% to 1.7% in August 2025.The government may be waiting for better timing to announce the change officially, possibly aligning it with broader fiscal reforms or budget announcements.

-

1 Like

For a small pension pot (<£10k) lump sum withdrawal, HMRC considers that 25% is a UK tax free amount, and the remaining 75% is regarded as ordinary earned income. A pension provider will normally take tax off at the basic rate (20%) on the 75% that remains.The entire amount will still of course be taxed in France.

I recall reading the debates about raising the ceiling for Livret A and the argument that this would cost the govt too much in tax-free interest (rough explanation..)

1 Like

I should clarify my own post above, I was talking about LEPs not Livret As regarding the inheritance but would not be surprised to learn that the same applies.

??? Has the “up to 3* pots of up to £10k taxfree in a lifetime” “Small Pots Exemption” gone, then? UK residents had the right to this taxfree but not well publicised and was one of the things an IFA knew about to suggest.

Or is the provider still obliged to withhold standard rate of tax ie about 20%, or worse yet, emergency tax even though the end position for a UK resident would have been up to £30k taxfree.

1 Like

It looks to me that’s it’s mandatory deduction at source (the pension fund holder) and you have to claim the tax back if you are able due to not working and not using your allowance.

Currently, 25% is UK tax free, 75% taxable as ordinary income, with PAYE being withheld at 20% basic rate of tax. There is no tax free (100%) exemption.

Here is a brief summary FYI from standard life.

Not emergency rate for small pots, just 20%. The UK £30k tax free exemption is for termination payments, rather than for pensions.

Hope this helps!

1 Like

There was a tax free exemption for up to 3 pots in a lifetime, each of up to £10k. It had to be specifically requested as a “small pots withdrawal” from a provider that knew how to do the admin (not all did) at the time of withdrawal. Last time I looked it was still available, I would guess around 2020 or so.

That meant a couple could withdraw £60k taxfree between them if they optimised the exemption.

1 Like

Not sure it’s still available but will check as it’s an important part of plans for possibly next year

If the question is whether 100% tax free Small Pots exemptions exist, I refer the Honourable Gentleman to the replies above..Sadly there is no 100% tax free exemption for Small Pots, just the usual 25% UK tax free amount. I’m actually not sure what real advantages, taking Small Pots now really amounts to, given you can take lump sums from most schemes, with a tax free element.

1 Like