Hi, the links I found have a lawyer who claims it back from the tax people.

Good luck!

Hi, the links I found have a lawyer who claims it back from the tax people.

Good luck!

So you have owned it for 20+ years? So you will have an exemption of 90% of the tax, and nearly 25% f the social charges anyway…… unless you have discovered a gold mine in the grounds I imagine the increase in value is not massive, so perhaps only worth an letter to the tax authorities and then move on to other things!

We are still waiting for out 2017 De Ruyter refund….

Same with me, I did a translation proof read for a Swiss company about to publish a book in English that first appeared in German because it was my area of expertise (though some here would dispute that ![]() ) The amount was €100 and was paid to me with a German cheque. I suppose the taxman felt sorry for me as the bloody bank ‘stole’ €30 of it.

) The amount was €100 and was paid to me with a German cheque. I suppose the taxman felt sorry for me as the bloody bank ‘stole’ €30 of it. ![]()

I have just sold a property in the UK (at last… I had hoped to sell it within a year of moving, but that did not happen). Although it was our family home for over 7 years, I then let it out for some years, so it was tenanted up until shortly before exchange of contracts.

So:

I have paid CGT in the UK…

I had to calculate a value for CGT as of 5th April 2015. To do this I subscribed to valuations calculated on that date for the 6 properties built to the same design at much the same time in the same small street. This was via Hometrack (you can put in a specific date for valuation such as April 2015) www.hometrack.com/uk/products/market-intelligence/property-valuation-report/

In the outcome the best GT result of the 3 possible ways of calculating it in the UK was theStraight Line Apportionment Method - pro-rata percentage between the year of purchase (2000) up to 2015, compared to 2015 to 2021. This worked out at 70% to 30% according to the HMRC simulator. So I could discount the gain by 70%. That meant that in fact the valuation at 2015 was meaningless, but still had to be calculated and entered in the CGT return. However the HMRC CGT return does not appear to take account of the Straight Line Apportionment Method! I ended up having to ring the HMRC helpline, and was put through to a "technician!. I was eventually advised to enter the pro-rata deduction under Other Reliefs using Straight Line Apportionment Method as the title.

CGT in France.

As I understand the situation I should get a credit in France for the payment to HMRC, but the capital gain will still affect our overall income for 2021, and there will be a balance of tax to pay if the tax due in France is more than the credit for tax in the UK.

I sent calculations etc to the local Impots, with all the attachments from the HMRC process. It was unclear to me how I translated the Euro value of a payment made in GBP in 2000 to calculate the Plus-Value. If I make the rate that prevailing on the actual date in 2000, then I have far less gain than if I make the rate that prevailing on the date of sale last month. I have tried the former and hope to see if it is challenged. (In every submission to the Impots I have always used the actual rate prevailing on the day of the transaction, and not the average for the year, so there is a “logical” precedent!)

I initially thought I probably had to use a Notaire to sort out the bills in France. However it appears that it is only necessary as far as I can see to make a return to the Impots within a month of the sale, using the 2021 version of form 2048-IMM-SD. That is not necessary if the CGT due in France is less than 15000 euros, although I assume tax will still be due and payable in the return for 2021 mid next year.

I suspect I now have an interesting wait to see if either set of calculations is challenged by either set of tax authorities!

I would very much appreciate any thoughts or suggestions!

Thank you for setting out your experience - it will be interesting to see if the tax office here reacts. They didn’t at all to the sale of my share of my mother’s house (stupidly didn’t’ do it straight away but left it for several years. One forgets here that one can accrue a capital gain in the UK quite quickly!).

They also didn’t even suggest I needed to pay social charges. If you are below state retirement age it will be interesting to see if that pops up or not.

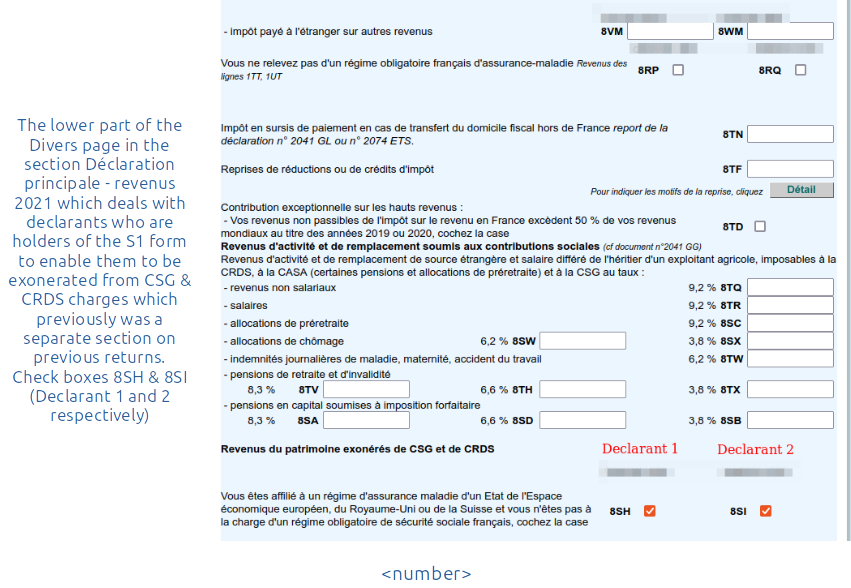

I’m over retirement age, and I have a form S1 so will specifically ask about the 7.5% solidarity payment vs the usual social charges.

Well, I’ve had an `interesting’ time following up the various links that many of you have kindly provided.

My head hurts.

I think I’m now clear on the original “De Ruyter” exemptions and that they apply up to 31/12/20. It would also seem that these exemptions are EEA only and have therefore ended for UK residents from 1/1/21 (DGFiP para 5) . The Aloy document confirms this although I agree with @ larkswood12 that the term individuals is ambiguous.

I also worked through the notes to formulaire No.2048-IMM which was quoted by the Notaire as to the reason they applied the full charge of 17.2%.

(1) : Les prélèvements sociaux sont dus au taux global de 17,2 %. Exception : les personnes qui ne sont pas affiliées au régime obligatoire français de sécurité sociale mais qui relèvent d’un régime de sécurité sociale d’un autre état membre de l’Union européenne, de l’EEE ou de la Suisse sont exonérées de CSG et de CRDS. En revanche, ces personnes restent redevables du prélèvement de solidarité de 7,5 % prévu à l’article 235 ter du CGI. Le Royaume-Uni ne fait plus partie de l’Union européenne ni de l’EEE depuis le 1er janvier 2021.

The Notaires office even queried this on our behalf with “someone at the top of the tax system(!)”, and came back adamant that the full amount was due. Dead end there I think.

It would seem the next stage is track down the WA and check out articles 30 & 31 as per the very useful FPN links (thank you).

Yes, “a letter to the tax authorities” is the reason for my original post. I was hoping that others might have had similar experiences and be able to guide me as to who to write to (eg local tax office or central department) and with what information (ie quoting what legal source etc). The amount involved is about 1700 Euros so worth a try I thought.

You say you are still waiting for a refund - may I what process you went through to apply for it?

As you know, The issue is that the UK is no longer part of the EU, so case closed for anyone who has moved to France since 31/12/20 and for people who are UK residents. But we have special status by virtue of the Withdrawal Agreement, so those of us with an S1 get the protection in perpetuity as long as we remain resident. But how to prove this? Every reference I’ve looked at cites articles 30 and 31 of the Withdrawal Agreement, but they don’t make a huge heap of sense!

For our previous overcharged social charges we have just been sending messages via our espace particulier….which gets a standard “we!re looking into it” reponse.

If I look at a gouv.fr document about social security changes for french people living in the UK is specifies there will be no changes - so why not the reverse.

Thanks so much for that link - most encouraging. As you say - if the French Gov can spell it out clearly for their citizens in UK, we must be able to find something similar over here!

I dipped a toe in to the WA agreement, found Articles 30 & 31, and glazed over (who writes this sh…stuff?). Even worse, I looked up the referenced EC n°883/2004 and EC n°987/2009 - they helpfully give a choice of every EU language with which to view them, but mine seemed to be firmly stuck between Greek and Double Dutch so I’m no further forward yet… (No wonder they pay lawyers the big bucks!)

I’ll have another go a bit later…

I have just sent an email to the British Embassy to ask for clarification about the continuing exemption. Won’t hold my breath, but I now have the bit between my teeth in this one! We have yet even had an offer on our flat, but best to be prepared!

Excellent!

This whole issue must surely have a potential effect on hundreds of UK S1-ers who have any form of investment income and who up till now have just ticked the box to automatically get the exemption.

It would seem that we know how this should now be treated, but forewarned is forearmed, and we just have to find how best to present our case to the “powers that be” in French Bureauland.

An update.

I filled in and sent Form No.2048-IMM to the Impots (no Notaire or Lawyer needed), with a cheque for CGT and Social Charges at 19.2% (as instructed by my local Impots - more on their interpretation after).

I attached a letter in protest, referring to “My rights to always be treated as a European citizen are fully protected by the “Withdrawal Agreement” - Exit Treaty of 24/1/2020, in particular article 31 on the coordination of social security which states that “the rules and objectives set out in Article 48 of the TFEU, Regulation (EC) No 883/2004 and Regulation (EC) No 987/2009 of the European Parliament and of the Council apply to the persons covered by this title. In the event of a conflict between the law of an EU Member State and the Withdrawal Agreement ”- Exit Treaty, the treaty must be honoured by the EU Member State, i.e. the treaty has priority.”

I received a reply shortly before Christmas, stating that the agency to which my local Impots instructed it be sent were not competent to deal with this, and it had been escalated to the “Pôle Gestion Fiscale de la Direction départementale des Finances publiques”. The cheque remains uncashed, and I am still waiting on a reply.

My local Impots particular interpretation was:

"Restent passibles de l’ensemble des prélèvements sociaux sur leurs revenus en capital :

I would be interested in any advice anyone has to continue to battle this!

I should note there seems to be a similar discussion on the facebook site Strictly Fiscal France - Strictly Fiscal France (facebook.com)

We are not getting far with our notaire, so I am planning to write to the EU commission to seek their view. The British Embassy interpretation was that this is a tax, and taxes are outside the withdrawal agreement….

I wonder whether the Embassy has any lawyers on its staff? suspect it may not!

@JoCo , look at the other CSG thread as you should now claim your money back!!

For info, this popped into my inbox yesterday from Blevins confirming S1 social charges exemption and 7.5% rate on interest and including capital gains post Brexit.

Perfect timing @larkswood12 as I was just lookingfor an appropriate thread to pose a question (or 2) regarding the S1. Apologies if my post is long and I will be talking to CPAM but hopefully someone might have been through a similar experience.

I also want to publicly thank @graham for his direct advice by private message which I have followed.

On Monday afternoon this week I spoke with NHS Business Services Authority regarding eligibility of S1 certificates for both myself and my wife having both now past the official age for receipt of UK state pension. Up until 2020 tax year our payable Social Charges here were quite acceptable but for 2021 this changed after my wife came of age for a UK state pension.

In addition to my UK state pension I receive a much smaller French pension and the fact that I do, no matter how small barrs me from being granted an S1.

On the other hand my wife does qualify for an S1 and following a long conversation on Monday afternoon received a confirmation email of acceptance. The S1 has arrived by post today!! Hats off to the NHS.

So now we have to present the S1 to CPAM.

What concerns me is that we have both had our cart vitales for 14 years andI am hopeful that in presenting the S1 it wiul merely be a case of changing my wifes current Code Gestion from 12 (General Scheme insured non contributors) to what I believe will be code 70 without the need to suspend, cancel or renew hee current carte vitale.

Of course my situation remains the same.

Finally as my wifes S1is backdated to when she qualified forher UK pension I am hopeful that our social charges liabilty for 2021 will be adjusted downwards.

Info from anyone with personal experience of general knowledge of the above situation is most welcome.

Apologies for spelling errors as spell check doesnt work on SF.

Spell checker works for me using SF and Firefox… do you just get no suggestions or they are inappropriate?

Thanks for the heads-up on the result of your ministrations with the NHS Business Agency. So pleased it was useful.

I do think that is the case… you don’t need to do anything other than register the S1 with CPAM and as to whether they change the code on the CV is mute.

The other issue is the tax submission just made. You need to contact the Fisc and have them note that your submission needs to be updated with the information that the S1 exists for your wife.