Hi everyone,

I’m posting that here because that’s a question I get a lot and I thought it could be great to share this.

To understand the percentages you need to understand how the system works, so ready your scuba gear and let’s deep dive.

In France, the social security has defined something like an Index (the BRSS in French - Base de Remboursement de la sécurité sociale that we can translate into Social Security Refund Rate). That index varies depending on the claim that’s being made and sometimes the index itself is calculated specifically given the circumstances but I’ll focus on “standard” cases. In general, the French SS refund 70% of their index (but that also can vary a lot, some medications can be refunded 15% for example) so when you have a 100% Mutuelle they refund 30% of the index (BRSS) and if you have a 200% policy then you can get refunded up to 2 times the index, etc.

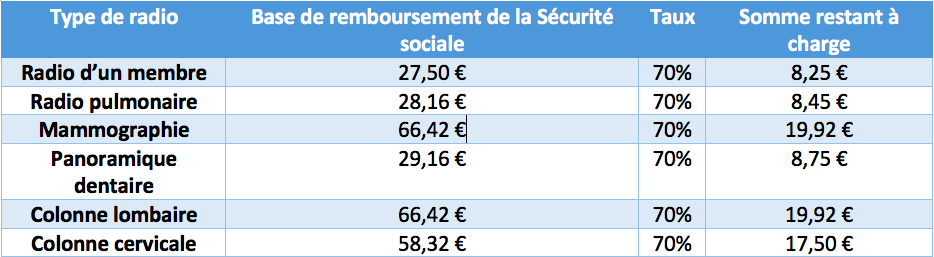

So let’s take an example of an x-ray (radio in French), the BRSS for x-rays in France goes as follows:

Let’s imagine you are going to the lab for an arm x-ray and let’s imagine that the lab charge 35€ for that.

The refund would then be 27,50 (BRSS) * 70% = 19,25€ so you’d be left to pay 35e - 19,25 = 15,75e. That 15,75e is what can be potentially compensated by the Mutuelle so let’s image a couple scenarios as follows:

As you can see, the financial burden that lies on you mostly depends on the spread between the BRSS and the fee they (doctors, labs, etc.) charge you. That’s actually why it is of paramount importance to favour “conventioned” doctors if you want to pay as little as possible (as they are committed to charge as close to the index as possible).

As it would be too easy if everything worked that way we also some “index free” kind of claim where the amount refunded is actually based on the real expense (and not an index). These claims are the hospitalisation itself and the medicine at the pharmacy. When you buy some medicine or are hospitalised then, with a Mutuelle, 100% of the medicine is refunded (as long as it’s taken in charge by the SS) and all hospitalisations are 100% covered whatever the cause (at least the stay at the hospital, the food, medicine, equipment and the potential surgery).

Hope that article answers some (unspoken) questions? Happy to answer some more if there is still some light to be shed on that topic