Good day all!

US citizen filing first French tax return on paper.

I have a “simple” return. US pension/Social Security income. I also have some dividends and interest, but my question is about where to input the pension income.

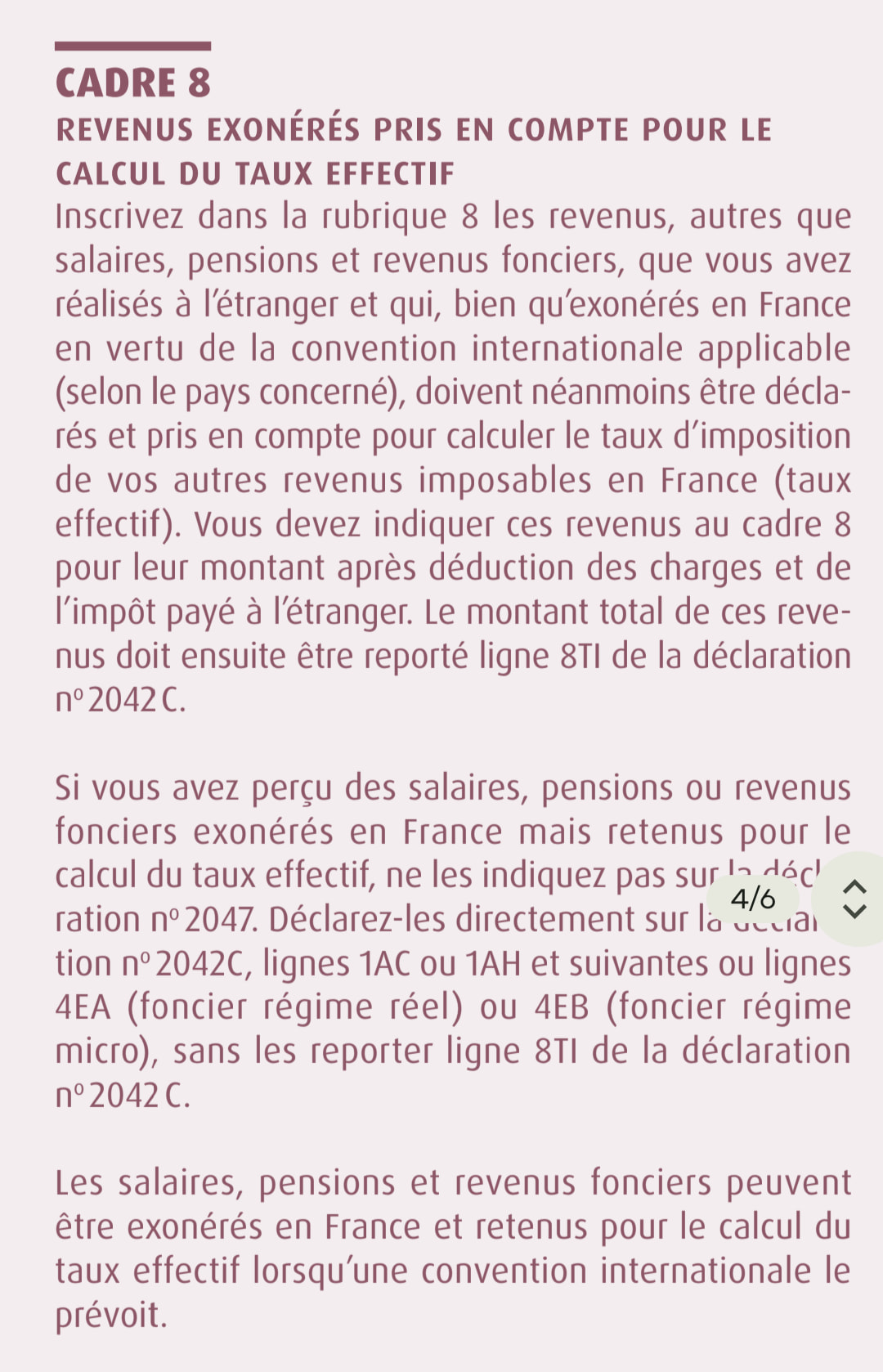

I was advised to complete for 2047: line 12 for the pensions, Section 2 for dividends and interest, then Section 6 for ALL the revenue sources including my US pensions, and -and here is the controversy>> Section 8 for the pensions exemption. This seemed like double counting to me, putting the pensions in 6 and also in 8. The 2047 form Notes says do NOT use section 8 for pensions. But tax “experts” on FB say YES, for US pensions, also add them to section 8, because they are exempt, but still use the main 2042 tax form, not 2042c, and add all income to line 8TK on the 2042.

For 2042, Section 1/1AL for the pensions, Section 2 line 2TS and 2TR for Div’s and Int. Then ALL the revenue on section 8 line 8TK. Straightforward.

>>>unless I really need to add 2042c, and that is if I am supposed to be declaring my US pensions in Section 8 of 2027.

For the TLDR crowd:

- On form 2047 do I input my US pension in Section 6 AND 8, or just 6?

- If YES, use both sections, then do I have to complete 2042c in addition to 2042?

Anyone know the answer here? TIA!

I had a slightly more complicated return with both US and UK pensions so for my first return I made an appointment with the local tax office (in Nontron in my case) and took all my information with me, They walked me through the various forms and were really helpful. Made it much simpler in subsequent years.

2 Likes

So who was it who advised you???

I second the benefit of visiting your Tax Office !

1 Like

I gave up working on declarations for today, but I’ll look tomorrow where I have put them for the last 3 years. Seems like 6 and 8 is the right answer.

If the exprts you are referring to are Childs and Miller on Facebook, then follow their advice. You have a very simple return. Going to the tax office is likely to confuse both them and you unless they are very familiar with the US-France tax treaty. I spent several hours with them my first year, and ,although I didn’t get bad answers, it was just easier to follow the crowd if you just have those 3 elements. No 2042c.

EDIT: Wrong. Only in 6 is where they are noted to be remove dper double taxation(also Section 1)

2 Likes

Thank you. I will still add the pension to Section 8 of the 2047, apparently this tells them not to attach Social charges to it?

Or calculates how much you should pay?

Sadly what they have done to me.

1 Like

One thing I do know is that for US pensions there are no social charges attached.

Interesting, do you know why that is? After making a mistake in my choice of boxes to use I have been accused of not contributing towards the system from which I have had good service. This is regarding UK pensions.

1 Like

I don’t know why they are attaching social charges, but maybe that is why the pension income needs to go in Section 8.

OH UK, different. Sorry I can’t help you there. Different tax treaty.

Articles 18.1 and 24.2 of the Franco / American tax treaty are the relevant provisions in answer to this issue. US pension income, whether Social Security or private in nature, received by a US citizen resident in France is only taxable in the USA. However, this income must be declared to the French tax authority, and so in order to avoid double taxation it is granted a French tax credit equal to the amount of tax that would have been payable were it to be taxed in France. Therefore it should be entered in Section 6, and ONLY Section 6, of the French 2047 form.

Section 8 of the 2047 form clearly states that this section must NOT be used for pensions.

Very happy to send you a copy of the Treaty if you wish.

2 Likes

Additionally, I can confirm that French Social Charges are NOT payable on US pension income, nor on US dividends and interest received by a US citizen resident in France. The French Ministry of Finance have long since accepted that Social Charges are just income tax by another name, and so Article 18 of the treaty applies. By the way, IRA withdrawals are also regarded as pension income.

Send me a PM and I can walk you through exactly what to enter in which boxes on which forms. The end result will be no French Tax or Social Charges payable.

2 Likes

I share your (very clear) analysis.

For what it’s worth, more or less the same question arose on the UK/France treaty recently. It seems the 2047 guidance around section 8 is both ambiguous and somewhat unhelpful, suggesting that [US, UK] pensions shouldn’t be on 2047 at all but reported on 2042C/1AC-1AH. See below.This is in conflict with the guidance elsewhere in 2047 which clearly states - for the US and UK treaties - such pensions should be reported in 2047 sections 1 & 6, and 1AL/8TK on 2042 to obtain the appropriate French tax credit/eliminate double taxation. My interpretation then, as now, is that the latter approach aligns most closely with the US/UK treaty wording and is absolutely the recommended approach.

2 Likes

Thank you! I understand where the items go now - there was just that point of confusion. It is interesting that you should say that dividends and interest are also not subject to social charges because there’s a lot of chatter on Facebook posts about people from the US being surprised to find dividends and interest absolutely being attached and charged. Apparently it depends on who looks at your tax return?

Unfortunately, and this has always been the case, there is wide variance between the various regional tax offices of the understanding of the provisions of the Franco / American treaty.

I have in my possession a copy of an official letter from the French Ministry of Finance situated in Bercy, Paris, that clearly states that French Social Charges are regarded as income tax for the purposes of said Treaty.

I can send you a copy if you wish.

A summation of the overall position is as follows, but please note that these provisions are only applicable to American citizens resident in France who retain their American citizenship and who have submitted, and paid, a US Federal tax return in relation to the relevant US income.

The following US income is effectively exempt from French taxation.

Pensions, whether Social Security or private, and including IRA withdrawals.

Dividends and Interest from investments held predominently in US companies and held / managed by a US investment house.

Capital Gains resulting from the sale of assets which have been generating the dividends and interest just mentioned.

I find that the best way to achieve the desired result is to submit the French tax return on paper forms, enclose a Mention Express that the relevant Articles of the Franco / American treaty apply, and enclose a copy of the ‘Bercy’ letter to guide their understanding.

Make sure that the tax return is correct in every respect and drown them in paper with lots of 3916 forms for the various foreign accounts, not forgetting the investment house accounts.

They will quickly recognise that you probably know more about the Treaty than they do and will do as they are told.

If you have any problems then do please let me know.

Just to be clear, I am not a professional tax adviser, but I do have many years experience of submitting both US Federal and French tax returns.

2 Likes

There is a box at the bottom of the 2042 where I always reference the treaty and the specific Sections that apply to my declaration wrt pensions, dividends and interest. There is also a space to write a note in the online version, whenever you do that. It is always best to lead the bureaucrats to the correct (0€) answer.

And Robert and George are correct ( only section 6) after looking at my declaration today. I had deleted all that from my brain yesterday when I quit for the day.

3 Likes

Thank you very much! Yes please do send me a copy of the Bercy letter.

Thank you. I will add the note as well as attach the letter along with my cover letter, as this is (obviously!) my first return.

If you look at the French form instructions for the 2047 (2047NOT pg 5 ) it reads:

UNITED STATES div. 17.6%, int. 17.6%

Dividends: Dividends from U.S. sources received by a resident of France entitle the recipient to a tax credit equal to the U.S. tax, up to a limit of 15% of the gross amount of the dividends. However, certain dividends from U.S. sources received by persons resident in France who are also U.S. citizens entitle the recipient, under the conditions stipulated in Article 24 § 1-b-i) of the Franco-American tax treaty of August 31, 1994, to a tax credit equal to the amount of French tax corresponding to this income, and not to the tax credit equal to the U.S. tax capped at 15%.

Interest: Interest from U.S. sources received by a resident of France entitles the recipient to a tax credit equal to the U.S. tax, up to a limit of 15% of the gross amount of the interest. Thus, if this interest was exempt in the United States, it does not entitle the holder to any tax credit in France. However, certain interest from US sources received by French residents with US citizenship entitles them, under the conditions stipulated in Article 24 § 1-b-i) of the Franco-American tax treaty of August 31, 1994, to a tax credit equal to the amount of French tax corresponding to this income, and not to the tax credit equal to the US tax capped at 15%.

1 Like