By pure chance I noticed a post elsewhere regarding a driver who was insured with Direct Assuurance, and whose claim was refused because his vehicle was right-hand drive. He was informed that Direct Assurance did not insure right-hand drive vehicles.

My car has been insured with Direct Insurance since November last year. They had photographs of every aspect of the car. There was no mention by them, nor did they ask, about right-hand drive vehicles when I completed the application.

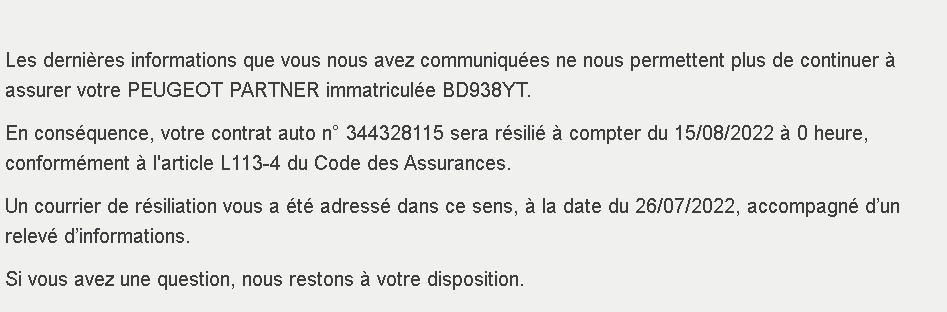

I wrote to them today asking them to clarify, and they have replied that the insurance is invalid and the vehicle will no longer be covered by them from next month.

I regard it as very fortunate discovering this, purely by chance, before I needed to make a claim!

Wow!

Do they express an opinion as to their reasoning?

Is the company French or English and would you consider approaching @fabien to continue your cover?

Hi @graham and @SuKe , what an unpleasant experience indeed. Direct Assurance is a French company underwritten by AXA but it’s part of the many “low cost” companies which always come with small prints unfortunately. I must admit I wasn’t aware of this either and that’s actually the first time I’ve heard of this type of exclusion. I would love to see the terms & conditions if you could ask them for a “motivation circonstanciée de la résiliation” that would be brilliant and I would love to have a look at it. I’m certain they are within “their rights” but that’s really unusual nethertheless. I’ve had to deal with countless claims with various insurers in France and right hand drive vehicle without any issue so far so I would be all in for a deeper investigation if I can assist you in any ways?

Ask them for an extract from their terms & conditions (conditions générales ou conditions particulière) which pin point this. In France we’re ruled by “Napoleon’s law” which goes like => if something is not explicitly excluded it is therefore covered (many examples of this during COVID / lockdowns where AXA had to pay massive loss of income to customers as they forgot to include that specific exclusion).

Ive had my RHD car insured by AXA since 2018. They know absolutely that it is a RHD car, as that was pointed out to them when we first met, and we were assured that it was no problem. I think it is also stated RHD on the policy. I will have to check this.

I will find an extract of their terms and conditions. I do wonder if they should refund the premiums I have been paying them since last November, seeing as the insurance was invalid.

Thanks for this, I can’t find any particular mention of the exclusion of right hand drive vehicles. I’ve also found this online which is an extract of a court judgment ruling out the right hand drive as a fault from the driver or a contradiction with French regulations. So I’m twice as curious to see who they justify this from a legal standpoint => https://www.lecomparateurassurance.com/103367-textes-loi/109124-accident-volant-droite-responsabilite-conducteur

I am quite shocked by Direct Assurance, because had I not come across a post on Facebook by somebody who had a similar problem with them, I’d never have known and could have been in a very difficult situation. Surely they should be compelled, in their application form, to include some mention of this particular exclusion?

Yes I should think you’d be entitled. We were mis-sold an insurance in France against our protests by a tied agent and when I had time to complain directly to the insurance co they spontaneously refunded all the premiums.

When we bought our current LHD Renault Espace in the UK 8 years ago and on UK plates, I checked with UK insurers and several would not insure an LHD vehicle. Most car insurers have a rule that any modifications must be notified to them and even small modifications that have no bearing on the vehicle safety or performance can be taken to have invalidated the insurance. Caveat Emptor is often the case with insurance - I accept a vehicle constructed as RHD or LHD cannot be considered to be modified from a logical perspective but legally it may not be so simple - legal matters so rarely are.

Direct online insurers are a potential minefield. Their business model is built on making things simple and “efficient” but that comes at a cost, which is that they focus on non-specialist cases in order to make the bulk business that they depend upon for that model. In many insurers, non-standard cases are judged separately and premiums adjusted accordingly where they accept the risk, but not these direct insurers who work mainly to computer algorithms. When I took out my UK insurance LHD or RHD was not mentioned on comparison sites and it was only later when I checked that I discovered this exclusion. (The car is since re-registered and insured here and of course without that problem).

And, actually, let’s be honest, there is an increased risk involved in driving an LHD vehicle in the UK or an RHD vehicle in France. Whether you choose to overtake on a single carriageway road ahead or not, your view of the road is more restricted.

Again legally, most insurers would have difficulty wriggling out of paying third party claims following an accident if they had been fully informed of the risk and accepted it anyway, even if their acceptance was based on their own negligence, but fully comprehensive cover might still be forfeited. In theory, therefore, you might have a valid claim for retrospective refund on the difference between third party and comprehensive insurance (which is often not a huge amount) but if it was contested I wouldn’t be confident of winning. Some companies will make a goodwill offer whilst maintaining they are not liable and that is the best hope IMHO.

Not wishing to be a party-pooper, I think that clause 16 (declaration of risks and subsequent modifications) does give them cover for their position. I am less familiar with the carte-grise layout but I can’t see anything there that conveys the information that the vehicle is LHD or RHD (neither does the UK equivalent, the V5C). Insurers would therefore presumably argue that they are entitled to consider that a French registered vehicle is LHD unless advised to the contrary and I suspect they would win that argument.

As I say in another post here, you could argue that a vehicle constructed with RHD is not a modification but I suspect that would not hold in court (especially against an insurer who can afford the best legal representation). I seem to recall that most UK insurers would not insure an LHD vehicle or required a substantial additional premium when I looked at this 8 years ago (I eventually insured with Saga who did not charge a premium but they were the exception not the norm amongst the companies I checked).

I don’t intend to take any action against them other than to ask them nicely to return the premiums paid. The amount is negligible and I don’t have the time, energy or inclination to get involved in a dispute.

I originally said the car had been insured with Direct Insurance since last November. I’ve realised that isn’t quite correct. My previous car was insured with them from November (it was LHD), but after it was killed it was replaced with the current car in March, only five months ago.

The reason for my original post was to warn others who may not be aware.

And I for one thank you for that. I have been a ‘leftie’ for many years now so it doesn’t apply but, for our first dozen years we did have a RHD Saxo re-registered in France, and it certainly never occurred to me at the time that it might not be covered.

BTW @Russellgww I agree with most of what you say but do dispute the claim that:

And, actually, let’s be honest, there is an increased risk involved in driving an LHD vehicle in the UK or an RHD vehicle in France. Whether you choose to overtake on a single carriageway road ahead or not, your view of the road is more restricted.

Apart from overtaking a large vehicle on a single carriageway there is little difference in my extensive experience of left hookers in UK or right hookers in France with regard to risk. I used to enjoy the Saxo and, following large vehicules apart, you can see through or (including with large vehicules) down the nearside. In fact it could be said that Macron did us a favour in that respect because so many HGV drivers stuck to the 90 on their limiters while we were legally bound to stay behind at 80. In fact it was so prevalent that I wondered if there was an exception for convictions where ‘livelihood’ was involved in the manner of the old ‘white’ permis for drunken convicted HGV drivers.

I know this argument has bee done to death on SF and other fora but I really can’t see the point in using a RHD vehicle for your daily drive in any LHD country…

When we had made the decision to move to France, one of the first things we did was to buy a LHD car (from a Brit returning to UK from France) as I considered it the safest option.

I understand the argument that UK cars tend to be cheaper to buy, but really, what price safety?

Crossed with my edit on the safety issue Graham but our reason for persisting with the Saxo was that in those early years we simply couldn’t afford a change.

Your logic is sound but France legal system works differently than countries under “common law”. The world is basically divided in two different legal system (western world at least). One being the common law (US, UK, Australia, etc.) and the other being “Napoleon law” (there may be another name but hey… French bias as it was first drafted by the guy ).

Under Napoleon law things need to be explicitly excluded otherwise you cannot use it against the customer that’s why I was wondering where exactly it says that it’s excluded (either in the terms and conditions or in the policy itself). I agree with you that it’s probably written somewhere otherwise they would not act like this but still it’s super unusual.

For information, I’ve double checked with the 30+ companies I’m working with and none have such exclusions so I’m really curious about that “case”. I’ll follow this closely

but our reason for persisting with the Saxo was that in those early years we simply couldn’t afford a change.

but our reason for persisting with the Saxo was that in those early years we simply couldn’t afford a change.