Yes the dreaded 30 day ceiling. I fell foul of that some years ago because I didn’t know of its existance. I was asked to transport a dog for the Dobie Association but my car wasn’t available at the time but, as it was urgent, they authorised me to hire one from Super-U.

I paid for the hire with my bank card but then made the mistake of putting the large covering deposit on it also. As that was refundable I thought no more about it but then I couldn’t use the card for a long period, so all other payments during that time had to be paid for with my English card, not a good idea. Of course what I should have done was put the deposit on the English one and only the real French expenses on the French one.

I wonder if getting an American Express card would be helpful for those who need to buy big-ticket items occasionally?

I got one many years ago (just the basic Green Card) specifically for emergencies like missing a flight and needing to buy a ticket at the last minute. With Amex the amount you can spend without pre-authorisation varies depending on your past spending pattern I believe, but there is no pre-set amount. You can phone them up and get a prospective purchase approved. I do this if I’m planning to buy something pricey like a new camera.

Just a thought, assuming they work the same way in France…

Can you still not do this online with CA? I gave up on them long ago, as, just like @_Brian, after Nth horrendous experience with Touraine-Poitou i just closed it down rather than give them another penny for no value whatsoever, so I’m not aware of current features but stuff like that should be pretty standard features in the app in 2025. I know BNP / Hello Bank let you automatically increase it in the app for 30 days without having to deal with customer services which is great, similar to the likes of Monzo and Starling in the UK which will allow you to increase the limits in app for 24 hours if you’re buying a car, house or whatever and need a little bit more.

The problem is that each region has its own version of CA with its own rules. I have an account with CA Touraine Poitou but over the last few years have migrated most of my banking over to a Fintech (with a French iBan etc) with whom I am very happy. I have kept the CA account to pay the house insurance by prélevement, and just in case I needed local banking support.

However, I’m about to cancel the account as I’m fed up of making a monthly payment for an account that I don’t think I need any longer. I am sure there are regions who offer an excellent service through CA - but I don’t think I live in one!

From what people tell me Centre Ouest is better, which is annoying as my notaire was in Le Dorat so I could’ve gone there to open it, but instead went to Montmorillon and got stuck with Touraine Poitou.

Partially, if the Credit Agricole Ma Banque app is feeling generous. You’ll see from the screenshot that you can -for “free”(!) - raise your limit - as a one-off till the end of the month…wow!

Thank you to everyone who has replied to my question.

Jim told the person at Credit Agricole that it was not a good time for him to spend answering their questions, but no one has rung back.

We do know that Banks now have a duty to get to know their customers, but if they do ring back we will ask them to send a copy of the relevant EU law.

Getting to know your customer works both ways as we are now much more aware of CA.

We had such a problem with our car insurance with them some years ago that we took all our insurances away from them.

We did ask them to increase the credit card limit they first gave us when we moved to France as we needed to buy large electrical items andbtgey did raise our limit.

This is the key. The banks absolutely have a duty to know their customers, the onus is on them, not the customer. They can ask you anything they want, and you as the customers can decide whether to answer (and face the risk of your account being closed, money frozen etc). The banks have become very good at wording it so that customers believe that tax authorities etc insist they give over all this information and if you don’t you’ll get in trouble when the reality is that it’s them, not you who would. As long as you reported everything to the authorities directly you’re good. Whether people want to squabble this point or just give them what they ask for so they go away is another matter altogether, but as we’re seeing in this thread even, this important questions they must know they answer to often turn out to not be so important or essential after all if you just say no…

We had a similar request from CA which was not even our main account/bank. It was couched as an obligatory annual patrimoine review. They wanted to know salary and other income details as well as assets (house etc ). I refused to answer, they kept insisting. Eventually I did as some others here have said and requested the reference of the legislation. No answer!

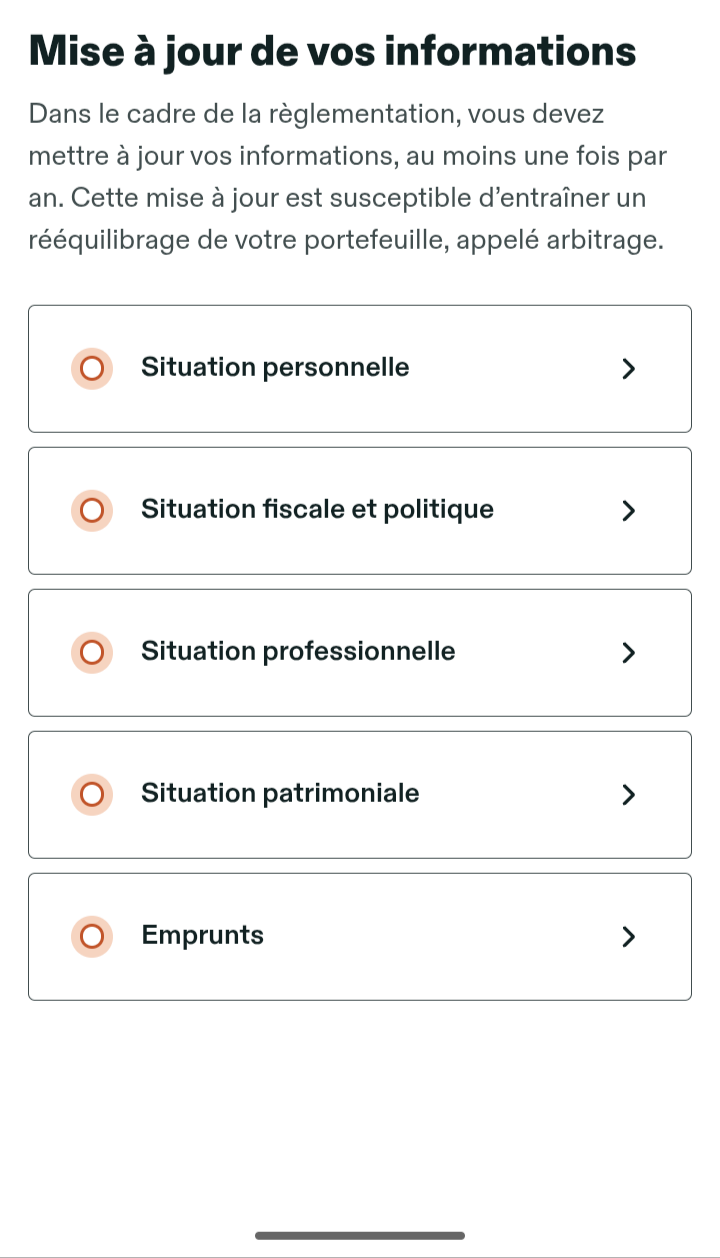

By complete coincidence I’ve just received this from my Assurance Vie provider, insisting that I need to update them annually on the value of our house/joint incomes/whether politically exposed/value of all other savings/tax residence, and citing “regulatory” requirements.

They’ve previously informed me that it’s the insurance regulator who pressurises the insurer who holds the client funds to know their clients, who in turn then pressurises the investor, ie me!

I’ve banked with CA Britline since they opened and well before we bought our house and moved here. They have never been anything other than helpful and I’ve never had any intrusive questions. When my husband died 4 years ago Britline, and my conseiller in particular , couldn’t do enough to help. This info is just a balance to all the ’ CA is crap ’ posts on here

Yes, I’ve heard good reports of Britline, but in making my criticisms I am aware that CA is a regional and not a national bank and my experience has only ever been of the one in this area.

That would be far too invasive for me. I’ve two AVs with HSBC, now through CCF, that I set up fifteen years ago. If they ever wanted that amount of irrelevant information, especially annually, (which I am reasonably confident they never will) I’d liquidate them and move the cash offshore.

The fact that there is no consistency between institutions (and from what I read above, in the case of CA, even within institutions) indicates to me that they are just winging it. It’s the old French banking model, the client exists to serve the bank, not the other way around.

Reading the many experiences here, it’s noticeable that several of the longer term clients of various banks, insurers etc have clearly not been troubled by the sorts of detailed questions that have been directed at more recent clients.

I vaguely recall the (UK) financial services industry informal practice (hotly denied, of course) that in order not to ‘inconvenience’ valuable, established clients, it was customary to rely on the position that since X had been a client for [25+] years, there was more than enough information on file to justify a reasonable conclusion that X was not a money laundering risk. Less established, ie more recent clients, were treated much more rigorously. It’s not impossible that there is a similar informal practice here in France.