On tax rates it states " Le projet de loiindexe le barème de l’impôt sur le revenu sur l’inflation (+1,8%),

and searching for rates a connexions table came up

2024 bands for 2023 income

2025 bands for 2024 income

Rates

Up to €11,294

Up to €11,509

0 %

€11,295 to €28,797

€11,510 to €29,344

11 %

€28,798 to €82,341

€29,345 to €83,905

30 %

€82,342 to €177,106

€83,906 to €180,471

41%

The temporary 20% minimum effective rate on high revenues (think pension lump sums) is confirmed and the conditions for eligibility to the Micro BIC regime applicable to furnished lettings have been further amended. More here - (though states 2% tax band uplift not 1.8)

Can someone clarify something for me as I have always been under the tax threshold but with my pension now kicking in it has taken me over the 0% limit. So, do I then pay tax on the difference between the low 0% upto my limit on the next band or is it taxed at the rate mentioned whatever I have in income from the beg to last figure in the next band? In other words, am I allowed upto the limit and then pay for what is just over that.??

Oh thank you very much indeed, I did think that would be the case but not sure and now I know I will be able to pay it in one go when its due. I have 33years of tax returns for France but as the business plus family was offset aggainst it we never had anything to pay and then for years on my own, I never got above €7k/year. I’m glad you understood my ramblings but I do worry when it comes to money matters.

I see the PS have put down a Budget amendment denying a capital gains tax exemption on the sale of a main residence if the owner hasn’t lived in it for at least 5 years. There are proposed exemptions for ‘hardship’ sales (eg going into an EHPAD, séparation etc) or a sale followed by a proposed acquisition that will also be a main residence. No idea if the idea will be adopted (probably not?) but it shows a policy approach that may yet be influential in the future.

(Apologies for updating the thread title to include 2026).

I wonder what the thinking is behind that. It doesn’t strike me that “flipping” properties (the sort of thing you might expect Socialists to target) is a big thing in France but maybe I’m wrong. Surely it’s just going to further hamper labour mobility.

I would have thought they would be more tempted by the kind of moves hinted at in the UK towards removing the CGT exemption for primary residences above a certain value.

The authors of the amendment are indeed targeting ‘flipping’ especially in tourist hotspots where the shortage of properties to rent is driving up prices significantly. They cite the Pays Basque in particular.…

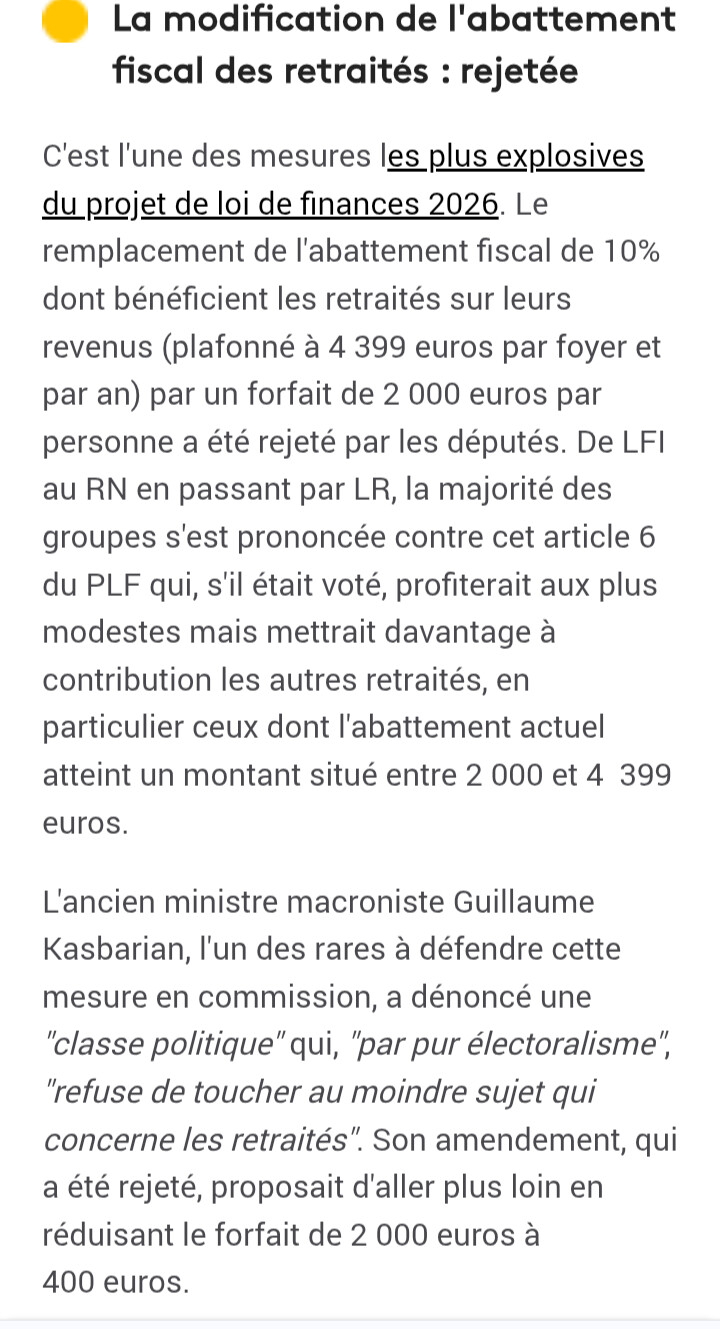

The French Parliamentary commission reviewing the draft budget for 2026 has thrown out the Government’s proposal to reduce the 10% allowance (abattement fiscal de 10%) for pensions with a fixed allowance of €2000.

The Assemblée nationale is now focusing on expanding the scope of the existing wealth tax (IFI) to an ”Impôts sur la fortune improductive”.This new proposed tax was passed at first reading with a very strange set of political bedfellows - the RN voting for it with MoDem and the PS….. Voted on yesterday, this new tax would include other items, of potential interest to SF members, such as “l’assurance-vie pour les fonds non alloués à l’investissement productif”, however that might be defined. The threshold for this new tax would be €1.3m with rates up to 1%ish.

There is a long way to go before any of this becomes final, with scope for multiple changes. The inclusion of Assurance vie (however defined) is likely to be controversial, given its popularity as a favoured savings vehicle amongst French voters. The government remains firmly opposed to any effective ‘reintroduction’ of the previous wealth tax, ISF. The latter was radically narrowed in scope by Macron after his first election to focus primarily on property rather than total wealth.

Sounds like they’re copying the UK in seeking to impose a “Lifetime Allowance” on Assurances Vie.

The problem is that if inflation / interest rates increase or if the currency value falls, all of which tend to happen if one does, then the Lifetime Allowance / any AV ceiling won’t buy enough pension in real terms. As the ISF threshold is unlikely to be indexed, just as LTA wasn’t.

On AVs, it appears that the deputés are targeting funds held within AVs that are basically Euro deposits, generating interest,.(presumably deemed “unproductive”) as opposed to the funds held in unit linked investments (deemed “productive”). “Only” the excess in wealth (on yachts, property, other unproductive assets etc) in excess of €1.3m would be taxed (ie there is no ‘all or nothing’ approach) at 1%. There is also a proposal to exclude €1m of a single asset for each household from the charge.

So, after issues trying to move retirement age up from 62 amid protests, government wants to save money by axeing the Cheistmas Bonus paid to people on hardship benefits like RSA. Apparently the plan is not to pay the Chriatmas bonus to those without children as part of their home.

It’s one thing to consider is this fair - after all why should you be entitled to Christmas if you don’t have children? and does it make sense. I was just taken by the amounts of the Christmas bonus which for a single person with no children at home currently on these benefits is 152 euros, or for a couple with no children at home the Christmas bonus is 228 euros. Presumably those on benefits with children at home will keep the bonus, and it sounds like for them it’s substantially more than these amounts.

I’m just thinking back to the UK, does anyone on benefits get a Christmas bonus at all ?

Article text that poppd up sbout this : “Attribuée à environ 2,5 millions de ménages, la prime exceptionnelle de fin d’année est réservée aux bénéficiaires du revenu de solidarité active (RSA), de l’allocation de solidarité spécifique (ASS) et de l’allocation équivalent retraite (AER). L’an dernier, son montant pour les foyers percevant le RSA s’élevait à 152,45 euros pour une personne seule sans enfant et à 228,68 euros pour un couple sans enfant.”