If I was to build up a substantial property portfolio of unfurnished apartments in France and receive 100k Euro yearly in rent, what would my approximate tax and social security outlay be? This would be my only worldwide income. Régime réel would apply I understand

I have tried to use the online calculators I have found, but have not been able to figure out how to use them correctly when the only income is rental income

Depends on a number of factors. Are you, or will you be, a UK state pensioner? As that reduces liability for social charges. Then depends on structure of your business, as income is one thing but you are taxed on profit. So will you have a structure that means you can offset depreciation for example? So need to work that through on number of units, initial investment etc. Also remember that currently property is subject to a wealth tax. So if the portfolio is worth more than 1.3million which it may well be to get that turnover, then you will pay an extra wealth tax each year.

As a hugely rough finger in the air ballpark I would guess a turnover of 100k would safely give you a €30k income.

Thank you for your reply!

I will not get a pension from anywhere. I have been moving around too much and never paid into any pension funds.

Not at the stage yet where I decide on private holding or through a company. Will pay for professional advice when/if I get to that stage. For now, I just want to get a feeling of whether moving and investing in France is feasible at all. I like the 10% return you can get in smaller towns.

But you are saying that I might end up spending 70% on tax and Social Security? Blimey, I knew France was a high tax country but that is insane

No, what I am saying is that €100k turnover is just turnover. From that you have to deduct all the costs and charges, plus maintenance etc etc. This includes things like the business tax - CFE. Which could bring you down to say 50 or 60k. On which you will pay tax around 30% and social charges of 19.2% and then possibly a further 0.5% on the value of the property itself.

However if when you say €100k income you mean your actual gross profit, then you will be paying 41% tax plus 19.2% social charges, plus more likely 0.7% on the portfolio.

10% return on investment is quite optimistic these days.

Ok thank you for clarifying. I meant 100k profit.

Is the social charges on the full 100k, or on what is left after taxes have been paid? I hope the latter, otherwise the total burden is over 60%. Even the former means over 52%

The 10% return would be after my own labour in renovating the properties.

Tax and social charges are imposed on the sum remaining after allowable expenses etc have been deducted. So if tax is due on 50k, then social charges are due on 50k. The only exemption is if you have a European nationality (no longer includes British) and your healthcare is paid for by another state, or you pay for your own health care via private insurance. Which would initially be much cheaper, but has other disbenefits.

No, I mean that I would buy a rundown property which is not rentable at the moment. After renovating it myself I would be able to get 14% return before costs due to the low purchase price and only paying for materials cost of the renovation. My time is given zero value in this scenario as it would be something for me to do.

Just my opinion based on the little info that has been offered.

Given the amount of money needed to generate 100K in gross profit Andy would be better just living off the capital until death unless they’re desperate to pass on a massive inheritance, that way they’ll be no income tax or social charges to pay.

I think what he means is 10% return on actual investment, which if he does the work himself would mean this higher return.

However, Andy, unless you are a registered and qualified tradesman you can’t then claim the costs of the work against any future capital gains. You can’t renovate and flip houses for profit here the way you can in some countries. A very different market.

I personally feel that 1 million in property is a safer bet than 1 million in shares etc but each to their own. If the share market would have it’s long overdue crash that would change my perception, but will that happen tomorrow or in 20 years?

I am past my flipping years. Not worried about capital gains tax as the plan would be to never sell. So the government would take most of it anyway as inheritence tax.

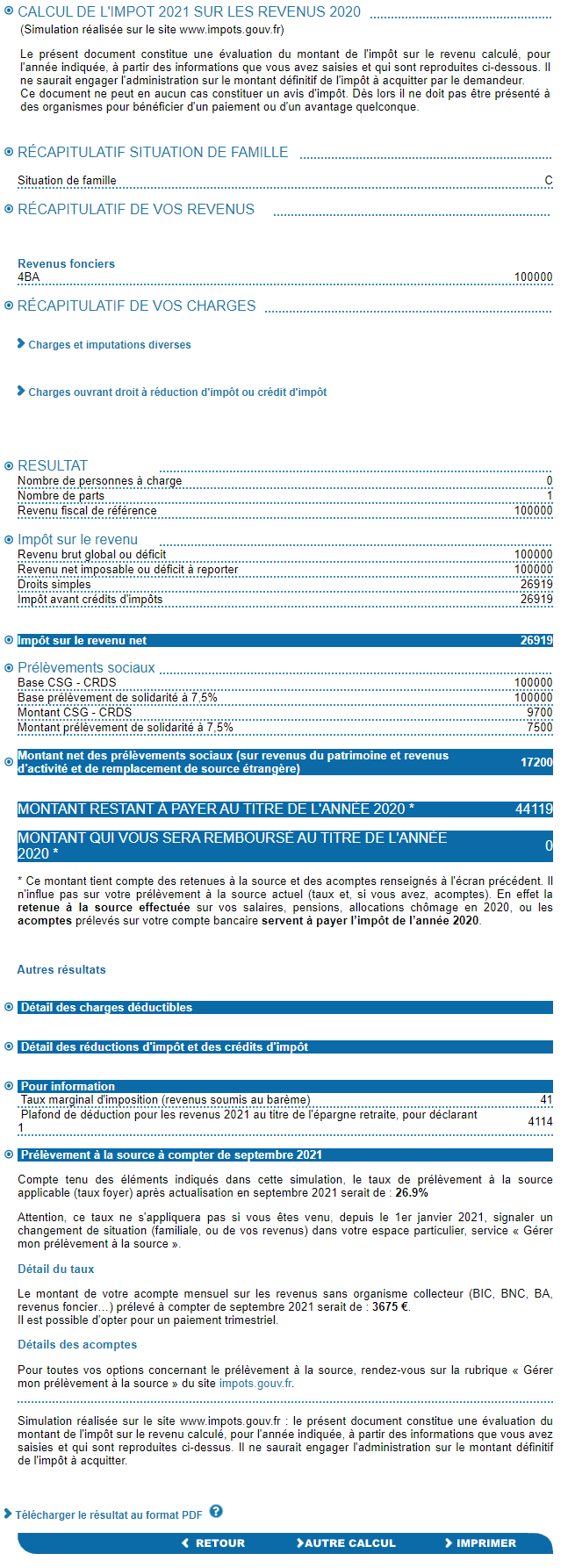

I found this calculator at impots.gouv.fr

I don’t know if I entered the rental income in the right box (4BA) but that one gives a total tax and social security burden of “only” 44.12%

Am I missing something?

Yes this might be doable in places, but I would say you would need to research the areas very carefully to get that return. 5% is often considered the average here.

Quite possibly not as I was giving ballpark figures. There is a sliding scale for tax, so0% on first bit, 11% on next slice etc etc and goes up to 40% over around 75k.

Who said anything about shares or the stock market? A million in pounds or euros would give you a handsome annual income free of tax and social charges for two or three decades. Obviously I don’t know your age but if you’re close to retirement age it’s certainly a way to guarantee an income for life.

That’s pretty much how it works in France.

The social charges are applied before tax when you are working, as opposed to being retired, which means that the burden is approximately 50-60%. @JaneJones assessment is pretty spot on, speaking from my own experience as an independent.

I think that you should contact axiom avocats in Toulouse. Mr Fuzel speaks perfect English as he was bought up in the U.K. but is French. he will be able to advise you on all aspects. From what I am understanding Wealth tax is a big consideration as you will be taxed on any world wide property over around 85,000 ( i think) but you only have to declare if you have over 1,300,000€ This must be declared after 5 years of living in France. Mr Fuzel can do tax simulations for you. You will also be liable for all of the other taxes, income, social charges, impôt foncier on each property too. I think you would need to have a siret number and pay and annual enterprise tax as well all of the other taxes. I think that you could set up a company but from what I understand this is very complicated. Best to get professional advice as the French tax system seems to be complicated.

You could have rental properties in the U.K. you’d then be liable to U.K. taxes and would also have to do a French tax return but any taxes paid in the U.K. would be credited in French taxes. It gets a bit confusing as the U.K. tax year is April to April and the French tax year is Jan 1 to Jan 1. There are also more allowances on U.K. property rental income compared to French property rental income. If you want to do property rental in France best to do it in ski or beach areas but be aware that there are a lot of french rules in favour of the tenent, you can not repossess your property that easily if the tenents do not pay their rent especially in the winter, you can not evict them in the winter. Do you speak fluent french? If you don’t you could have a problem understanding all if the rules and regulations. If you let à property in France there is no necessity to provide a kitchen, a sink is sufficient. You could also use a french letting agency. Had you thought of doing short term let’s ie. rent your seaside house out in the summer and winter whilst the live in a mountain house. Depending on where you choose there can be a large market for this type of thing. Then there is the parts system fir income tax, are you alone or do you have a spouse or family? Linder

Investing in property would mean buying at the top of the market in either country and whilst I think the French market is less prone to ‘peaks and troughs’ the UK market is likely to dip once interest rate hikes start to bite.

Personally I don’t think it’s a good idea to base your retirement income on just one type of investment, a mix of property, cash and some sort of pension would be better.